Navigating the complexities of Indonesian tax law can feel daunting, but effective tax planning is crucial for both individuals and businesses. Understanding Perencanaan Pajak, or tax planning, is key to maximizing financial well-being and ensuring compliance. This guide provides a comprehensive overview of Indonesian tax laws, strategies for optimization, and the importance of accurate reporting. We’ll explore various tax planning techniques, address common concerns, and offer insights into future trends, empowering you to make informed financial decisions.

From understanding the core principles of effective tax planning and the various types of taxes applicable in Indonesia to developing strategies for individuals and businesses, this guide offers practical advice and real-world examples to illustrate key concepts. We will also delve into international tax considerations and the ever-evolving landscape of Indonesian tax policy.

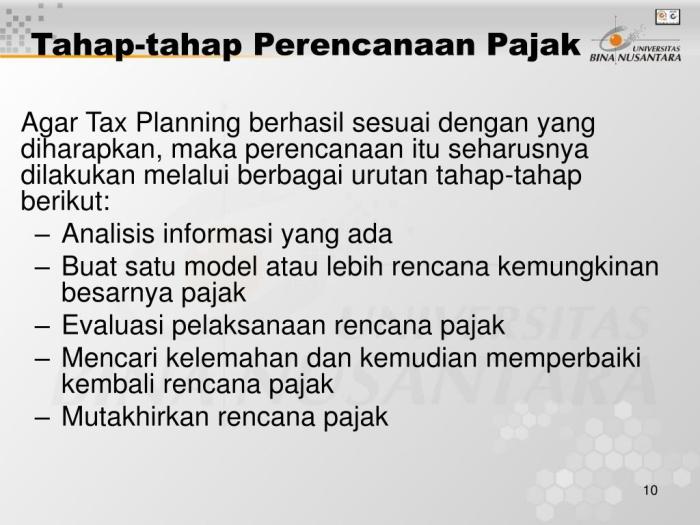

Understanding Perencanaan Pajak (Tax Planning)

Effective tax planning in Indonesia involves strategically managing financial activities to minimize tax liabilities while remaining compliant with the law. It’s a proactive approach, not a reactive one, focusing on long-term financial health rather than simply reacting to tax deadlines. Understanding the Indonesian tax system and utilizing available legal deductions and incentives are key components of successful tax planning.

Core Principles of Effective Tax Planning in Indonesia

Effective tax planning in Indonesia adheres to several core principles. Firstly, it prioritizes compliance with all relevant tax regulations. Secondly, it emphasizes a long-term perspective, considering the implications of current decisions on future tax obligations. Thirdly, it leverages available tax incentives and deductions to legally reduce tax burdens. Finally, it involves meticulous record-keeping and documentation to support tax filings and audits. Ignoring any of these principles can lead to penalties and legal issues.

Types of Taxes Applicable in Indonesia

Indonesia has a multi-tiered tax system encompassing various levies. These include Income Tax (Pajak Penghasilan or PPh), which applies to individuals and businesses; Value Added Tax (Pajak Pertambahan Nilai or PPN), a consumption tax; and Goods and Services Tax (Pajak Penjualan atas Barang Mewah or PPnBM), a luxury goods tax. Other taxes include Land and Building Tax (Pajak Bumi dan Bangunan or PBB), and various regional taxes. Each tax type has its own specific rates, thresholds, and reporting requirements. Understanding these distinctions is crucial for effective tax planning.

Common Tax Planning Strategies for Individuals and Businesses

Several common strategies can help individuals and businesses optimize their tax positions. For individuals, these include maximizing allowable deductions for education expenses, health insurance premiums, and charitable donations. Businesses can explore tax incentives for investment in certain sectors, research and development, and employee training programs. Both individuals and businesses can benefit from proper asset allocation to minimize tax exposure. Careful planning around investment timing and the utilization of tax-advantaged savings schemes are also valuable strategies.

Comparison of Tax Optimization Techniques

| Technique | Description | Individuals | Businesses |

|---|---|---|---|

| Tax Deductions | Utilizing allowable deductions to reduce taxable income. | Education, health, charity | Investment allowances, R&D expenses |

| Tax Credits | Direct reduction of tax liability. | Child tax credits (where applicable) | Tax holidays for specific industries |

| Tax-Advantaged Investments | Investing in assets or schemes with favorable tax treatment. | Retirement funds, certain bonds | Tax-free zones, infrastructure bonds |

| Strategic Asset Allocation | Optimizing asset holdings to minimize tax implications. | Diversification across different asset classes | Optimizing capital structure (debt vs. equity) |

Tax Laws and Regulations

Understanding Indonesian tax laws and regulations is crucial for effective tax planning. This section Artikels key aspects of the Indonesian tax system, recent legislative changes, potential compliance issues, and real-world examples illustrating legal interpretations. The Indonesian tax system is complex, requiring careful navigation to ensure compliance and minimize tax liabilities.

Indonesian tax laws are primarily governed by Law Number 7 of 1983 concerning Income Tax (as amended several times) and Law Number 8 of 1983 concerning Value Added Tax (VAT) and Sales Tax on Luxury Goods (SSTLG) (as amended several times). These laws, along with various implementing regulations and ministerial decrees, form the foundation of the Indonesian tax system. The system is broadly based on self-assessment, meaning taxpayers are responsible for calculating and paying their taxes accurately and on time.

Key Tax Laws and Regulations

The Indonesian tax system encompasses various taxes, including Income Tax (PPh), Value Added Tax (PPN), Sales Tax on Luxury Goods (PPnBM), Land and Building Tax (PBB), and others. Income tax applies to individuals and businesses, with different rates and regulations depending on income levels and business structures. VAT is a consumption tax levied on the supply of goods and services. PPnBM is levied on specific luxury goods. Understanding the specific rates and regulations for each tax type is vital for accurate tax planning. For example, the tax rates for corporate income tax vary depending on the company’s turnover, while personal income tax rates are progressive, increasing with higher income levels. Specific regulations also exist for different types of income, such as investment income, capital gains, and rental income.

Implications of Recent Tax Legislation Changes

Recent changes in Indonesian tax legislation, such as the Omnibus Law on Job Creation and subsequent implementing regulations, have introduced significant modifications to the tax system. These changes impact various aspects, including tax incentives, tax rates, and reporting requirements. For instance, some tax incentives have been restructured or removed, while others have been introduced to stimulate specific sectors of the economy. The implementation of electronic invoicing (e-invoicing) has also significantly altered reporting procedures, requiring businesses to adapt their systems to comply with the new regulations. These changes necessitate a thorough review of existing tax strategies to ensure continued compliance.

Potential Areas of Non-Compliance and Consequences

Potential areas of non-compliance include inaccurate reporting of income, improper claiming of deductions, failure to file tax returns on time, and incorrect calculation of tax liabilities. The consequences of non-compliance can be severe, ranging from penalties and interest charges to legal action and even imprisonment in serious cases. For example, late filing penalties can be substantial, and deliberate tax evasion can lead to significant fines and criminal prosecution. Maintaining accurate records and seeking professional tax advice are crucial to mitigate these risks.

Real-World Case Studies Illustrating Tax Law Interpretation

One example involves a multinational corporation that misclassified certain expenses, resulting in an underpayment of corporate income tax. This led to a lengthy audit and significant penalties. Another case involved an individual who failed to report rental income, leading to tax evasion charges and legal consequences. These cases highlight the importance of accurate record-keeping, proper tax classification, and seeking professional advice to ensure compliance with complex tax regulations. The details of specific cases are often confidential due to legal and privacy reasons; however, these examples illustrate the potential consequences of non-compliance.

Tax Planning Strategies for Individuals

Effective tax planning is crucial for individuals in Indonesia, especially high-income earners, to legally minimize their tax liabilities and maximize their financial well-being. This involves understanding the Indonesian tax system and strategically utilizing available deductions and investment options. Proper planning can significantly reduce the overall tax burden without compromising legal compliance.

Tax Planning Strategy for a High-Income Earner in Indonesia

A high-income earner in Indonesia can employ several strategies to optimize their tax position. These strategies often involve a combination of maximizing allowable deductions, strategically investing in tax-advantaged instruments, and carefully structuring income streams. For example, a high-earning individual might utilize a combination of retirement savings plans, charitable donations, and investments in government bonds to reduce their taxable income. Careful consideration of the types of income received (salary, business income, capital gains, etc.) is crucial for tailoring a personalized strategy. Professional tax advice is often recommended for individuals in this income bracket to navigate the complexities of the Indonesian tax code effectively.

Claiming Allowable Deductions for Individuals

Claiming allowable deductions is a key component of tax planning for individuals. This step-by-step guide Artikels the process:

- Gather Necessary Documents: Compile all relevant documents proving eligible expenses, such as receipts for education expenses, medical bills, and donations to registered charities. Accurate record-keeping is essential.

- Identify Eligible Deductions: Familiarize yourself with the types of deductions allowed under Indonesian tax law. These typically include expenses related to education, healthcare, and charitable contributions, along with certain business expenses for self-employed individuals. The specific allowable deductions and their limits are subject to change, so it’s crucial to consult the most up-to-date regulations.

- Prepare Tax Return: Accurately report all income and eligible deductions on the relevant tax forms. This requires careful calculation and attention to detail to ensure compliance.

- Submit Tax Return: Submit the completed tax return within the designated timeframe to the Indonesian tax authority (DJP). Late submissions can result in penalties.

- Maintain Records: Retain copies of all submitted documents for future reference in case of audits.

Minimizing Tax Liability Through Legitimate Means

Minimizing tax liability involves maximizing allowable deductions and strategically investing in tax-efficient instruments. This doesn’t involve tax evasion but rather using the legal framework to reduce the overall tax burden. For example, contributing to a pension fund reduces taxable income while simultaneously providing for future retirement security. Similarly, investing in certain types of bonds or mutual funds might offer tax advantages. Careful financial planning and consultation with a tax professional can help individuals navigate these complexities.

Investment Options for Tax Optimization

Investing strategically can significantly reduce your tax liability. Several options exist, each with its own set of tax implications:

- Retirement Funds (Dana Pensiun): Contributions to approved retirement funds are often tax-deductible, reducing your taxable income in the present while providing for retirement security.

- Government Bonds (Obligasi Negara): Certain government bonds might offer tax benefits, either through tax exemptions or reduced tax rates on the interest earned.

- Sharia-Compliant Investments: Investing in Sharia-compliant instruments can provide both financial returns and alignment with religious principles. Tax implications vary depending on the specific investment.

- Mutual Funds (Reksa Dana): Depending on the type of mutual fund, certain tax advantages might apply. It is crucial to understand the tax implications before investing.

- Insurance Premiums: Certain life insurance premiums may be deductible, reducing your taxable income. This needs to align with regulations governing deductible insurance premiums.

Tax Planning Strategies for Businesses

Effective tax planning is crucial for the long-term financial health of any Indonesian SME. By strategically managing tax obligations, businesses can maximize profitability, reinvest earnings, and ensure sustainable growth. This section Artikels key tax planning strategies specifically tailored for SMEs operating within the Indonesian context.

Tax Implications of Different Business Structures

Choosing the right business structure significantly impacts tax liabilities. In Indonesia, common structures include sole proprietorships, partnerships, and limited liability companies (PT). Sole proprietorships are the simplest, with business income directly taxed under the owner’s personal income tax. Partnerships, while offering some liability protection, typically face a similar tax treatment where each partner is taxed individually on their share of profits. Limited liability companies (PTs), on the other hand, are considered separate legal entities, subject to corporate income tax on their profits, offering stronger liability protection for the owners. The choice depends on factors like liability concerns, administrative complexity, and the desired level of tax optimization.

Tax Credits and Incentives for Businesses

The Indonesian government offers various tax credits and incentives to stimulate economic growth and support specific industries. These include deductions for research and development expenses, investments in certain capital goods, and tax holidays for businesses operating in designated regions. To claim these benefits, SMEs need to meticulously maintain accurate records, fulfill specific eligibility criteria, and submit the necessary documentation to the tax authorities. The availability and specifics of these incentives can change, so staying updated on the latest regulations is vital.

Depreciation Methods for Tax Purposes

Depreciation, the systematic allocation of an asset’s cost over its useful life, impacts a business’s taxable income. Indonesia allows several depreciation methods, each with its own implications. The straight-line method, the simplest, allocates an equal amount of depreciation each year. The declining balance method accelerates depreciation in the early years, leading to lower taxable income initially. The unit of production method bases depreciation on the asset’s actual usage. The choice of method depends on the asset’s nature and the desired tax outcome. Selecting the appropriate method requires careful consideration of the asset’s expected lifespan and usage patterns.

| Depreciation Method | Calculation | Advantages | Disadvantages |

|---|---|---|---|

| Straight-Line | (Cost – Salvage Value) / Useful Life | Simple to calculate; consistent depreciation expense. | May not reflect actual asset decline in value. |

| Declining Balance | (Book Value at Beginning of Year) x Depreciation Rate | Higher depreciation in early years, resulting in lower taxable income. | Can lead to lower depreciation expense in later years. |

| Units of Production | ((Cost – Salvage Value) / Total Units to be Produced) x Units Produced in Year | Reflects actual asset usage; more accurate depreciation. | Requires accurate tracking of asset usage. |

International Tax Considerations

Navigating the complex landscape of international taxation is crucial for Indonesian businesses with global reach. Understanding the interplay between Indonesian tax laws and international tax treaties is essential for optimizing tax efficiency and mitigating potential risks. This section will explore the key tax implications for Indonesian companies operating internationally, focusing on tax treaties, common challenges, and effective tax optimization strategies.

Indonesian businesses engaging in international operations face a unique set of tax challenges and opportunities. These stem from the diverse tax systems in different countries, varying regulations regarding cross-border transactions, and the need to comply with both Indonesian and foreign tax laws. Effective international tax planning requires a comprehensive understanding of these complexities and a proactive approach to minimizing tax liabilities while remaining compliant.

Tax Implications for Indonesian Businesses with International Operations

Indonesian businesses operating internationally are subject to both Indonesian tax laws and the tax laws of the countries where they operate. This can lead to double taxation, where the same income is taxed twice – once in Indonesia and once in the foreign jurisdiction. Profits earned from overseas operations, royalties, dividends received from foreign subsidiaries, and other cross-border transactions are all subject to specific tax rules and reporting requirements. Failure to comply with these regulations can result in significant penalties and legal repercussions. Proper structuring of international transactions and adherence to relevant tax treaties are vital for mitigating these risks.

Tax Treaties and Their Impact on Cross-Border Transactions

Tax treaties, also known as double taxation avoidance agreements (DTAAs), are bilateral agreements between countries to prevent double taxation of the same income. Indonesia has entered into numerous DTAAs with various countries, aiming to streamline cross-border transactions and provide certainty for businesses operating internationally. These treaties typically define the tax residency of individuals and companies, allocate taxing rights between countries, and provide mechanisms for resolving tax disputes. The specific provisions of each DTAAs vary, and understanding their implications is critical for efficient tax planning. For example, a DTAA might reduce the withholding tax rate on dividends or interest payments received from a foreign source.

Challenges and Opportunities Related to International Tax Planning

International tax planning presents both challenges and opportunities. Challenges include navigating complex tax regulations in multiple jurisdictions, managing transfer pricing issues (the pricing of goods, services, and intangible assets transferred between related entities), ensuring compliance with various reporting requirements, and dealing with potential tax audits in different countries. Opportunities arise from leveraging tax treaties to minimize tax liabilities, optimizing the location of business activities to benefit from favorable tax regimes, and strategically structuring international transactions to achieve greater tax efficiency.

Tax Optimization Strategies for Multinational Corporations Operating in Indonesia

Multinational corporations (MNCs) operating in Indonesia can employ several strategies to optimize their tax position. These strategies include structuring their operations to take advantage of tax incentives offered by the Indonesian government, utilizing transfer pricing strategies that comply with OECD guidelines, and strategically utilizing tax havens (though with careful consideration of ethical and legal implications). Proper tax planning can lead to significant cost savings and enhanced profitability. For example, an MNC might establish a regional headquarters in Indonesia to benefit from tax incentives related to foreign investment, or it might structure its supply chain to minimize import duties and other taxes. However, it is crucial that all tax optimization strategies remain compliant with both Indonesian and international tax laws. Careful consideration of BEPS (Base Erosion and Profit Shifting) initiatives is also paramount.

Tax Compliance and Reporting

Ensuring tax compliance in Indonesia is crucial for businesses and individuals alike. Understanding the process of filing tax returns, potential penalties for non-compliance, and the role of tax professionals are key to navigating the Indonesian tax system effectively. This section details the practical aspects of tax compliance and reporting within the Indonesian context.

Filing Tax Returns in Indonesia

The process of filing tax returns in Indonesia varies depending on the taxpayer’s status (individual or business) and the type of tax involved (income tax, VAT, etc.). Generally, it involves accessing the online tax system, DJP Online (Direktorat Jenderal Pajak Online), completing the relevant forms, uploading supporting documentation, and submitting the return electronically before the designated deadline. Taxpayers are assigned a unique taxpayer identification number (NPWP) which is essential for all tax-related transactions. Specific instructions and forms are available on the official DJP website. Failure to file on time results in penalties. The process may require assistance from tax professionals, particularly for complex tax situations.

Penalties for Non-Compliance with Tax Regulations

Non-compliance with Indonesian tax regulations carries significant penalties. These penalties can include fines, interest charges on unpaid taxes, and in severe cases, legal action. The severity of the penalty depends on the nature and extent of the non-compliance. For example, late filing typically incurs a late filing penalty, while tax evasion can lead to substantial fines and potential criminal charges. The Directorate General of Taxes (DJP) actively enforces tax regulations and investigates cases of non-compliance. Accurate record-keeping and timely filing are crucial to avoid these penalties.

Role of Tax Consultants and Advisors

Tax consultants and advisors play a vital role in ensuring tax compliance. They provide expertise in interpreting complex tax laws and regulations, assisting with tax planning, preparing tax returns, and representing taxpayers in dealings with the DJP. Their services are particularly valuable for businesses and high-net-worth individuals with complex tax situations. Engaging a qualified tax professional can help minimize tax liabilities, ensure compliance with regulations, and reduce the risk of penalties. They can offer guidance on various tax strategies, ensuring optimal tax efficiency.

Checklist for Accurate Tax Reporting

Accurate tax reporting is essential for avoiding penalties and maintaining a positive tax standing. A well-organized approach is crucial. Here’s a checklist of essential steps:

- Maintain accurate and up-to-date financial records throughout the tax year. This includes invoices, receipts, bank statements, and other supporting documentation.

- Understand the applicable tax laws and regulations relevant to your specific situation (individual or business).

- Determine your tax liability accurately based on your income, expenses, and deductions.

- Prepare your tax return using the correct forms and following the instructions provided by the DJP.

- Double-check all information entered on your tax return for accuracy before submission.

- File your tax return electronically through DJP Online before the deadline.

- Retain copies of your tax return and supporting documentation for future reference.

- Consult a tax professional if you have any questions or require assistance.

Future Trends in Perencanaan Pajak

The Indonesian tax landscape is undergoing significant transformation, driven by technological advancements, evolving economic conditions, and global best practices. Understanding these future trends is crucial for effective tax planning, ensuring compliance, and optimizing tax efficiency. This section explores the key shifts anticipated in Perencanaan Pajak in Indonesia.

The Impact of Digitalization on Tax Administration

Digitalization is rapidly reshaping tax administration in Indonesia. The implementation of e-filing systems, online payment gateways, and data analytics tools is enhancing efficiency and transparency. For example, the Directorate General of Taxes (DGT) has invested heavily in developing its online tax services portal, simplifying the process for taxpayers to file returns and make payments. This digitalization reduces processing time, minimizes errors, and improves overall tax compliance. Furthermore, the increased use of data analytics allows the DGT to identify potential tax evasion more effectively, leading to improved revenue collection. The use of Artificial Intelligence (AI) and machine learning in identifying discrepancies and anomalies in tax filings is also becoming increasingly prevalent, demanding more sophisticated tax planning strategies from businesses and individuals.

The Evolving Landscape of Tax Policy in Indonesia

Indonesia’s tax policy is continuously evolving to address economic challenges and promote sustainable development. Recent policy shifts have focused on simplifying the tax system, broadening the tax base, and improving tax administration. For instance, the government has implemented various tax incentives to encourage investment in specific sectors, such as renewable energy and infrastructure. Simultaneously, there’s a growing emphasis on strengthening tax enforcement to combat tax evasion and improve revenue collection. These policy changes often necessitate adjustments in tax planning strategies to remain compliant and optimize tax benefits. For example, the introduction of new tax incentives might require businesses to restructure their operations to qualify for the benefits.

Emerging Challenges and Opportunities in Tax Planning

The changing tax landscape presents both challenges and opportunities for tax planning. One major challenge is keeping up with the rapid pace of legislative changes and technological advancements. Tax professionals need to constantly update their knowledge and skills to provide effective tax advice. However, this also presents opportunities. The increased use of technology allows for more sophisticated tax planning strategies, such as utilizing AI-powered tools to optimize tax efficiency. Furthermore, the government’s focus on simplifying the tax system can potentially reduce the complexity of tax planning, leading to cost savings for taxpayers. The growing importance of Environmental, Social, and Governance (ESG) factors is also influencing tax planning, as businesses increasingly seek to integrate ESG considerations into their tax strategies.

Potential Future Changes in Tax Legislation and Their Implications

Predicting future changes in tax legislation is inherently challenging, yet analyzing current trends provides valuable insight. Indonesia might see further simplification of the tax system, potentially through the consolidation of various taxes or the introduction of a more comprehensive tax code. There could also be increased scrutiny of international tax arrangements to combat tax avoidance by multinational corporations. This may involve stricter transfer pricing regulations or the implementation of measures to prevent base erosion and profit shifting (BEPS). These changes could significantly impact the tax planning strategies of multinational corporations operating in Indonesia, requiring them to adapt their structures and practices to ensure compliance. For example, companies might need to review their transfer pricing policies to ensure they align with the latest regulations and avoid penalties.

Wrap-Up

Mastering Perencanaan Pajak requires a proactive approach and a thorough understanding of the relevant laws and regulations. By implementing the strategies Artikeld in this guide and staying informed about future trends, individuals and businesses can significantly reduce their tax burden while maintaining full compliance. Remember, seeking professional advice is always recommended for complex tax situations to ensure optimal results and peace of mind.

Questions and Answers

What are the penalties for late tax filing in Indonesia?

Penalties for late tax filing in Indonesia vary depending on the type of tax and the length of the delay. They typically involve late payment interest and potentially administrative fines.

Can I deduct charitable donations from my taxable income?

Yes, under certain conditions, charitable donations are deductible from your taxable income. Specific regulations and limits apply; consult the latest tax guidelines for details.

How often are Indonesian tax laws updated?

Indonesian tax laws are regularly updated. Staying informed through official government channels and reputable tax publications is crucial for compliance.

What is the difference between a tax consultant and a tax advisor?

While the terms are often used interchangeably, a tax consultant typically provides general advice, while a tax advisor offers more specialized and in-depth support, often representing clients during audits.

{kind=link}