Estate Planning untuk Keluarga: Let’s face it, nobody wants to think about their own mortality, but crafting a solid estate plan isn’t just about avoiding awkward family squabbles over Grandma’s prized porcelain collection (though that’s a definite plus!). It’s about ensuring your loved ones are financially secure and emotionally supported long after you’ve traded in your earthly possessions for a celestial harp. This guide navigates the sometimes-murky waters of Indonesian estate law, offering a surprisingly entertaining journey through wills, trusts, and the delicate art of family communication – all while keeping your assets safe from hungry tax collectors.

We’ll delve into the intricacies of Indonesian inheritance laws, exploring the various types of wills and the best strategies for distributing your assets fairly and efficiently. We’ll also address the unique challenges faced by families with special needs members, ensuring everyone is provided for with dignity and care. Prepare to learn about tax minimization techniques that would make even the most seasoned accountant raise an eyebrow (in admiration, of course). Get ready to navigate the sometimes-tricky terrain of family dynamics, learning how to have those crucial conversations about inheritance without causing a full-blown family feud. And finally, we’ll even tackle the surprisingly complex world of digital assets – because let’s be honest, your online presence is as valuable as your physical possessions these days.

Understanding Estate Planning for Families in Indonesia

Navigating the world of Indonesian estate planning can feel like trying to assemble IKEA furniture without the instructions – challenging, potentially frustrating, but ultimately rewarding if you get it right. This section will illuminate the legal landscape and common pitfalls, offering a clearer path towards securing your family’s future.

The Legal Framework Governing Estate Planning in Indonesia

Indonesia’s estate planning is primarily governed by the Civil Code (Kitab Undang-Undang Hukum Perdata or KUHP) and the Inheritance Law (Undang-Undang Nomor 1 Tahun 1974). These laws dictate how assets are distributed after someone’s death, outlining the rights of heirs and the process of probate. Understanding these legal foundations is crucial, as deviating from them can lead to lengthy and costly legal battles – a situation best avoided, especially when dealing with emotionally charged family matters. Think of it as the rulebook for your family’s financial legacy; mastering it is key.

Types of Wills Available for Indonesian Families

Indonesian law recognizes several types of wills, each with its own advantages and disadvantages. The most common are holographic wills (written entirely in the testator’s handwriting), and attested wills (witnessed and notarized). A holographic will offers simplicity, but its validity can be challenged if handwriting authenticity is questioned. An attested will provides greater legal certainty, but requires the involvement of a notary public, adding to the cost and complexity. Choosing the right type depends on individual circumstances and comfort levels with legal formalities. Think of it as choosing between a quick sketch and a professionally framed masterpiece – both can represent your wishes, but one offers more legal protection.

Common Estate Planning Challenges Faced by Indonesian Families

Many Indonesian families grapple with unique challenges when planning their estates. These often include issues related to undocumented assets, complex family structures (especially with extended families and customary inheritance practices), and a lack of awareness regarding the legal process. Disputes over inheritance are unfortunately common, often stemming from unclear documentation or conflicting interpretations of customary law. Proper estate planning can mitigate these risks, creating a smoother transition for future generations. It’s like having a well-organized toolbox; the right tools make the job easier and less prone to errors.

Comparison of Traditional Inheritance Customs with Modern Estate Planning Practices

Traditional Indonesian inheritance customs, often rooted in adat (customary law), can differ significantly from modern estate planning practices based on the Civil Code. Traditional methods may prioritize lineage and kinship ties in a way that doesn’t always align with modern legal frameworks. Modern estate planning allows for greater flexibility and control over asset distribution, enabling individuals to tailor their wishes to specific needs and circumstances. The key is finding a balance that respects both tradition and legal requirements, ensuring a fair and efficient distribution of assets. Think of it as bridging the gap between age-old traditions and modern legal safeguards.

A Simple Flowchart Illustrating the Estate Planning Process in Indonesia

Imagine a flowchart with these stages: 1. Assessment: Identifying assets and liabilities. 2. Planning: Determining inheritance distribution according to wishes and legal requirements. 3. Documentation: Creating a will (holographic or attested) and other necessary legal documents. 4. Execution: Registering the will with the relevant authorities. 5. Implementation: The executor manages the estate and distributes assets according to the will after the testator’s death. This simple visual representation guides individuals through the essential steps, providing a structured approach to a complex process. It’s like a roadmap, guiding you through the sometimes-winding roads of estate planning.

Key Components of a Family Estate Plan: Estate Planning Untuk Keluarga

Let’s face it, nobody wants to think about their own mortality. But a well-structured estate plan isn’t just about avoiding awkward family squabbles after you’re gone; it’s about ensuring your loved ones are taken care of and your wishes are respected. Think of it as a sophisticated game of financial Tetris, where you strategically arrange your assets to avoid a chaotic collapse.

A comprehensive family estate plan in Indonesia involves more than just a will. It’s a multi-faceted strategy designed to protect your family’s financial future and ensure a smooth transition of your assets. Failing to plan properly can lead to unnecessary legal battles, tax burdens, and emotional distress for your heirs. So, buckle up, and let’s delve into the essential elements.

Appointing a Legal Executor and Guardian

Choosing the right executor and guardian is crucial. The executor is the person responsible for managing your estate after your death, paying off debts, and distributing assets according to your will. Think of them as your financial superhero, navigating the often-complex legal landscape. A guardian, on the other hand, is responsible for the care and upbringing of any minor children you may have. This person needs to be someone you trust implicitly with both your financial and parental responsibilities. Selecting individuals with strong organizational skills and a good understanding of financial matters is highly recommended. Consider factors like their reliability, trustworthiness, and ability to handle potential conflicts. Perhaps avoid appointing your eccentric uncle who believes in communicating with squirrels.

Asset Management and Fair Distribution Among Heirs

Distributing assets fairly among heirs can be a minefield, even with the best intentions. Clear instructions in your will are paramount. Specify exactly what each heir receives, and if possible, consider using a trust to manage assets for beneficiaries who may not be financially savvy. For example, a trust could be set up to manage a significant inheritance for a young adult, ensuring they receive funds responsibly over time. This prevents them from potentially squandering their inheritance in a moment of youthful exuberance (we’ve all been there!). Remember to consider the unique circumstances of each heir; what might be a boon for one might be a burden for another.

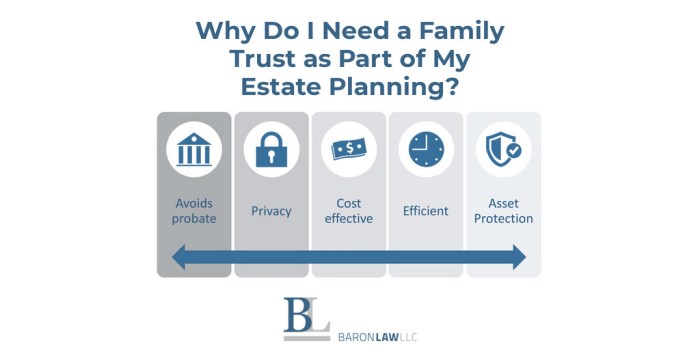

Protecting Family Assets from Creditors and Taxes

Protecting your hard-earned assets from creditors and excessive taxes is a key objective. Strategies like establishing trusts and utilizing life insurance policies can help shield assets from creditors’ claims. Additionally, proper tax planning, including understanding inheritance tax laws in Indonesia, is vital to minimizing the tax burden on your heirs. This isn’t about hiding money; it’s about legally minimizing financial liabilities to maximize what your family inherits. Think of it as playing the tax system strategically, like a sophisticated game of chess.

Comparison of Asset Types and Estate Planning Implications

Different asset types have different implications for estate planning. Understanding these differences is crucial for effective planning. Here’s a simplified comparison:

| Asset Type | Estate Planning Implications | Potential Issues | Mitigation Strategies |

|---|---|---|---|

| Real Estate | Can be complex to transfer; requires clear title documentation. | Property disputes, valuation challenges. | Clear title transfer instructions in the will, professional valuation. |

| Stocks and Bonds | Relatively easy to transfer; value can fluctuate. | Market volatility, potential for capital gains tax. | Diversification, tax-efficient investment strategies. |

| Bank Accounts | Generally easy to transfer; subject to probate. | Potential for freezing of accounts during probate. | Joint ownership, beneficiary designations. |

| Life Insurance | Passes directly to beneficiaries; avoids probate. | Policy terms and conditions must be carefully reviewed. | Ensure beneficiaries are clearly specified and up-to-date. |

Protecting Family Members with Special Needs

Estate planning gets a little more… *interesting* when you’re factoring in the needs of family members with disabilities. It’s not just about dividing up the family fortune like a particularly complicated game of Monopoly; it’s about ensuring the ongoing care and financial security of someone who might require lifelong support. Think of it as a sophisticated, legally-binding version of a very, very long-term care plan. And yes, it involves paperwork. Lots and lots of paperwork. But fear not, we’re here to navigate this slightly less-than-hilarious maze.

Protecting the assets intended for a family member with special needs requires careful planning and a deep understanding of relevant laws. The goal is to provide for their needs without jeopardizing their eligibility for government benefits like Supplemental Security Income (SSI) and Medicaid. These programs offer crucial financial assistance, and inadvertently disqualifying someone can have devastating consequences. This isn’t about avoiding taxes; it’s about ensuring your loved one receives the support they need to thrive.

Special Needs Trusts: A Lifeline for Long-Term Care

Special needs trusts are specifically designed to hold and manage assets for individuals with disabilities without impacting their eligibility for government benefits. These trusts are meticulously crafted to ensure that only the trust’s income, and sometimes a portion of the principal, is used to supplement the beneficiary’s needs, leaving the remaining assets protected. Think of it as a financial fortress, shielding assets while allowing for strategic disbursement. For example, a special needs trust could pay for things like adaptive equipment, specialized therapy, or even a comfortable home modification – all while keeping the beneficiary’s government benefits intact. This is crucial because relying solely on government benefits might not cover all expenses, and a well-structured trust fills that gap without jeopardizing the existing support system.

Strategies for Ensuring Long-Term Care and Financial Security

A robust estate plan for a family member with special needs will often incorporate several key strategies working in concert. These strategies are designed to create a multi-layered approach to financial security, providing a safety net that adapts to changing needs over time. One common strategy is establishing a supplemental needs trust in conjunction with a will or other estate planning documents. This ensures that the assets designated for the beneficiary’s care are managed appropriately, even after the death of the primary caregiver. Another critical aspect is designating a reliable and capable trustee, someone who understands the nuances of managing a special needs trust and advocating for the beneficiary’s best interests. This individual will play a crucial role in ensuring the trust’s funds are used effectively and ethically.

Legal Implications of Establishing a Special Needs Trust

Establishing a special needs trust involves navigating a complex legal landscape. It’s not a DIY project; you’ll need the expertise of an estate planning attorney experienced in this specific area. The attorney will guide you through the process, ensuring the trust is properly drafted to comply with all relevant laws and regulations. This includes understanding the distinctions between different types of special needs trusts (e.g., first-party vs. third-party trusts) and choosing the structure that best suits your family’s circumstances. Ignoring these legal complexities could lead to unforeseen problems down the line, potentially jeopardizing the very financial security you’re trying to create. The cost of legal expertise is a small price to pay for the peace of mind knowing your loved one is financially protected.

Steps Involved in Setting Up a Special Needs Trust

Before embarking on the process, it’s crucial to understand the complexities involved. A poorly constructed trust can lead to unintended consequences, so professional guidance is paramount. Remember, this is about securing your loved one’s future, not playing legal roulette.

- Consult with an estate planning attorney: This is the most critical first step. An experienced attorney will guide you through the process and ensure the trust is legally sound.

- Gather necessary information: This includes financial information, medical records, and details about the beneficiary’s needs and support system.

- Determine the trust’s structure: Choose between a first-party or third-party trust, depending on the source of the funds.

- Draft the trust document: The attorney will prepare the legal document outlining the trust’s terms and conditions.

- Fund the trust: Transfer the designated assets into the trust account.

- Appoint a trustee: Choose a responsible individual to manage the trust assets and ensure they are used for the beneficiary’s benefit.

- Regularly review and update the trust: Circumstances change, so periodic review ensures the trust remains relevant and effective.

Minimizing Estate Taxes and Legal Fees

Navigating the Indonesian estate tax landscape can feel like traversing a jungle teeming with tax-hungry jaguars and paperwork-wielding gorillas. But fear not, intrepid estate planner! With the right strategies, you can tame this wild terrain and significantly reduce the financial burden on your heirs. This section unveils the secrets to minimizing estate taxes and legal fees, transforming your estate planning journey from a perilous expedition into a smooth, efficient cruise.

Indonesia’s estate tax system, while potentially daunting, offers opportunities for strategic maneuvering. Understanding the tax implications of inheritance and estate transfer is crucial. The tax rate, applicable to the net value of the inherited assets, varies depending on the relationship between the deceased and the heir. Spouses and direct descendants generally receive more favorable treatment than other beneficiaries. Furthermore, certain assets, such as those designated for charitable purposes, may enjoy tax exemptions.

Inheritance Tax Rates and Exemptions

The inheritance tax rates in Indonesia are progressive, meaning higher values are taxed at higher rates. For example, a certain percentage might apply to the first IDR 500 million, while a higher percentage applies to the portion exceeding that amount. Specific rates are subject to change, so consulting a tax professional is always advisable. Importantly, various exemptions exist, potentially reducing the taxable estate value. These exemptions can significantly impact the overall tax burden, particularly for larger estates.

Strategies for Minimizing Estate Taxes

Minimizing estate taxes requires proactive planning. Several strategies can help reduce the overall tax liability. One common approach involves utilizing available exemptions and deductions to lower the taxable estate value. Another involves strategically structuring assets to minimize tax exposure. For instance, gifting assets during one’s lifetime (within legal limits) can reduce the value of the estate subject to inheritance tax. Remember, seeking professional advice from a tax specialist is paramount to ensure compliance and maximize tax benefits.

Tax-Efficient Estate Planning Techniques

Several tax-efficient techniques can significantly reduce the overall estate tax burden. These include establishing trusts, utilizing life insurance policies strategically, and making charitable donations. Trusts can help manage and distribute assets efficiently, often minimizing tax implications. Life insurance policies, when structured correctly, can provide liquidity to pay estate taxes without impacting the inheritance received by beneficiaries. Charitable donations, within legal limits, can reduce the taxable estate value and provide tax deductions.

Reducing Probate Costs and Administrative Expenses

Probate, the legal process of administering an estate after someone’s death, can be costly and time-consuming. However, several methods can help reduce these expenses. Creating a well-drafted will that clearly Artikels asset distribution is crucial. This minimizes potential disputes and streamlines the probate process. Additionally, establishing a living trust can avoid probate altogether, significantly reducing administrative costs and delays. A living trust allows for the transfer of assets directly to beneficiaries without going through the court system.

Comparison of Estate Planning Options

The costs associated with different estate planning options can vary significantly. The table below provides a simplified comparison, highlighting the potential cost differences. Remember that these are estimates and actual costs may vary depending on individual circumstances and the complexity of the estate.

| Estate Planning Option | Initial Cost | Ongoing Cost | Probate Cost |

|---|---|---|---|

| Simple Will | Low | None | Potentially High |

| Living Trust | Moderate to High | Low | Low to None |

| Complex Estate Plan (Trusts, Insurance, etc.) | High | Moderate | Very Low |

Communication and Family Dynamics in Estate Planning

Estate planning in Indonesia, while crucial for securing your family’s future, can often resemble navigating a minefield of emotional landmines and potentially explosive family disagreements. Open communication is the key to defusing these potential conflicts and ensuring a smooth transition of assets, preventing future family feuds that could make a Shakespearean tragedy look like a sitcom. Ignoring this aspect is akin to leaving a ticking time bomb under the family Christmas tree – best avoided.

The Importance of Open and Honest Family Communication Regarding Estate Planning

Open communication is paramount in estate planning. Failing to discuss your wishes openly can lead to misunderstandings, resentment, and protracted legal battles. Imagine the chaos: siblings fighting over the family heirloom batik collection, cousins squabbling over the beachfront property, all while the family lawyer charges exorbitant fees to untangle the mess. A proactive approach, however, fosters trust, transparency, and ultimately, peace of mind. It’s about setting clear expectations, preventing future conflicts, and ensuring everyone feels heard and respected. Think of it as preemptive damage control, saving everyone from a potentially expensive and emotionally draining legal battle.

Addressing Differing Opinions and Expectations

Family members often hold vastly different opinions and expectations regarding inheritance. Some may prioritize financial security, others might value sentimental possessions, while others may have entirely different priorities. These conflicting desires can create friction and tension, especially if the deceased hasn’t clearly articulated their wishes. A well-structured estate plan, however, can help mitigate these conflicts by clearly outlining asset distribution, ensuring fairness and transparency. This doesn’t mean everyone will be equally happy, but it does ensure a fair and transparent process. Consider a scenario where one child has supported the parents financially for years, while another has lived abroad. A well-structured plan will address such disparities and acknowledge unequal contributions.

Strategies for Facilitating Productive Conversations about Inheritance and Asset Distribution

Creating a safe and respectful environment for these discussions is crucial. Begin by acknowledging that everyone’s feelings and perspectives are valid, even if they differ. Using a neutral tone and avoiding accusatory language will help maintain a positive atmosphere. Employing active listening techniques – truly hearing and understanding what others say – is crucial. Consider scheduling a series of smaller meetings rather than one large, potentially overwhelming session. This allows for more focused discussions and avoids information overload. A visual aid, such as a simple chart showing assets and potential distributions, can also be helpful in clarifying expectations.

Benefits of Involving a Neutral Third Party

A neutral third party, such as a mediator or financial advisor, can be invaluable in facilitating these conversations. They provide an objective perspective, help manage conflicts, and ensure that everyone’s voice is heard. They act as a facilitator, guiding the conversation and helping to reach a consensus. This professional intervention prevents emotions from overriding logic and ensures the process remains focused on the family’s best interests. Their expertise also helps navigate complex financial and legal matters, ensuring a legally sound and ethically responsible distribution of assets.

Sample Family Meeting Agenda for Discussing Estate Planning Matters

A structured approach is vital for productive discussions. A sample agenda might include:

- Introductions and Icebreaker (setting a relaxed tone)

- Review of existing assets and liabilities (transparency and clarity)

- Discussion of the deceased’s wishes (understanding the plan)

- Open forum for questions and concerns (addressing anxieties)

- Brainstorming potential solutions to disagreements (collaborative problem-solving)

- Agreement on next steps (establishing a clear path forward)

This structured approach ensures all important aspects are covered, promoting clarity and preventing the meeting from becoming disorganized or emotionally charged. Remember, the goal is to foster understanding and cooperation, not to reignite long-dormant family rivalries.

Digital Assets and Estate Planning

Let’s face it, your digital life is now a significant part of your overall estate. From online banking accounts to cherished photo albums stored in the cloud, your digital footprint is worth considering when planning for the future. Ignoring this aspect is like leaving a significant portion of your legacy to the digital ether – a fate worse than a rogue email ending up in your grandma’s inbox.

Digital assets represent a surprisingly complex area of estate planning, often overlooked until it’s too late. The challenges involved in managing and transferring these assets are unique and often require proactive planning to avoid digital chaos for your loved ones. Think of it as a digital will, but with far more complicated implications than a simple handwritten testament.

Types of Digital Assets Included in an Estate Plan

A comprehensive estate plan should account for a broad range of digital assets. This includes online banking and investment accounts, email accounts and their associated contacts, social media profiles (because let’s be honest, some of those old Facebook posts are priceless…or horrifying, depending on your perspective), digital photographs and videos, domain names, online business accounts, and even cryptocurrency holdings. Failing to plan for these can lead to significant legal and emotional hurdles for your heirs.

Challenges in Managing and Transferring Digital Assets After Death

The biggest hurdle is often access. Many online services have robust security measures designed to protect user accounts, which unfortunately can make it incredibly difficult for heirs to gain access after death. Password recovery systems are often insufficient, and many platforms require legal documentation that can be challenging to obtain. Furthermore, the sheer volume and variety of digital assets can be overwhelming for grieving family members, making the process even more complicated. Imagine trying to untangle a digital Gordian knot made of forgotten passwords and confusing terms of service.

Strategies for Securing and Distributing Digital Assets to Heirs

One effective strategy is to create a comprehensive digital asset inventory, meticulously documenting every account, platform, and associated login information. This inventory should be stored securely, perhaps in a fireproof safe or encrypted digital vault, and clearly indicated within your overall estate plan. Another crucial step is designating beneficiaries for specific accounts whenever possible. This allows for a smoother transfer process, minimizing the need for lengthy legal battles. Consider using a trusted estate planning attorney who understands the intricacies of digital asset management. Think of them as your digital asset sheriffs, keeping order in the Wild West of online accounts.

Creating a Digital Asset Inventory and Access Plan

A well-structured digital asset inventory should include the account name, website URL, login credentials (stored securely, of course!), and contact information for the service provider. It should also specify which heir is to inherit each asset and any specific instructions regarding access or management. This plan should be regularly updated to reflect changes in your online life. Think of it as a digital household inventory, but instead of listing your silverware, you’re listing your cloud storage and cryptocurrency wallets. Don’t forget to include instructions on how to access and manage your email accounts – these often serve as a central hub for other important information.

Recommendations for Managing Online Accounts and Passwords

- Use a password manager to securely store and manage all your online credentials. Think of it as a high-tech, super-secure key ring for your digital life.

- Regularly update your passwords and utilize strong, unique passwords for each account. This is not the time for “password123” – your digital legacy deserves better.

- Inform a trusted individual of your digital asset inventory and access plan. Think of this person as your digital executor – someone who can help navigate the digital landscape after your passing.

- Consider utilizing a digital asset management service that specializes in securing and transferring digital assets after death. These services often offer specialized tools and expertise to simplify the process.

- Update your digital asset inventory and access plan at least annually, or whenever there are significant changes to your online accounts.

Illustrative Case Studies

Estate planning in Indonesia, while sometimes feeling like navigating a particularly thorny durian, can be surprisingly straightforward with the right guidance. Let’s explore a couple of scenarios to illustrate the potential pitfalls and the sweet rewards of proper planning.

The Case of the Contentious Cousins

Imagine the Budiman family. Patriarch Pak Budiman, a successful entrepreneur, passed away without a will. He left behind a thriving batik business, a sprawling villa in Bali, and three cousins with wildly differing opinions on everything from the best way to fold a batik sarong to the ideal shade of turquoise for a swimming pool. The ensuing family feud over the inheritance became a legendary saga, complete with whispered accusations, dramatic courtroom scenes, and a hefty legal bill that would have made Pak Budiman weep into his kopi. The lack of a clear estate plan resulted in protracted legal battles, strained family relationships, and a significant depletion of the family’s assets. The batik business, once a source of pride and prosperity, suffered greatly due to the uncertainty surrounding its ownership. The villa, a symbol of family unity, became a battleground.

Resolving the Budiman Family’s Estate Issues

The key to untangling this mess would have been a well-structured will. This document would have clearly Artikeld Pak Budiman’s wishes regarding the distribution of his assets, potentially specifying the management of the business and the allocation of the villa. Mediation could have been employed to help the cousins understand each other’s perspectives and find common ground. Had a trust been established, it could have overseen the management of the assets until a predetermined time, reducing the risk of immediate conflict. A clear division of assets, potentially with the involvement of a neutral party, could have prevented the protracted legal battle. The family’s financial losses, both direct and indirect, could have been significantly reduced. The outcome? A far less stressful experience, preserving family relationships and assets.

Lessons Learned from the Budiman Family

The Budiman family’s unfortunate experience underscores the critical need for comprehensive estate planning. A well-defined plan minimizes family conflict, protects assets, and ensures a smoother transition of wealth. The cost of neglecting estate planning far outweighs the cost of creating one. It’s a proactive approach that safeguards against future disputes and protects the legacy of the family.

The Case of the Tech-Savvy Widower

Now, let’s consider Pak Santoso, a software developer who passed away leaving behind a substantial digital estate – a highly valuable portfolio of cryptocurrency, intellectual property rights to several successful apps, and numerous online accounts. He was a loving husband and father of two, but his digital assets were not properly addressed in his will. His wife, Ibu Ratna, struggled to access his cryptocurrency holdings and was uncertain about the legal ownership of his apps. Accessing his online accounts proved to be a bureaucratic nightmare.

Managing Pak Santoso’s Digital Legacy, Estate Planning untuk Keluarga

The challenge here highlights the importance of addressing digital assets in estate planning. Pak Santoso should have created a digital asset inventory, clearly documenting all his online accounts, passwords, and ownership details. He could have designated beneficiaries for his digital assets and specified how they should be managed. A digital executor could have been appointed to manage the complex technical aspects of accessing and distributing the digital assets. His will should have included specific instructions for handling these assets, avoiding the lengthy and frustrating process that Ibu Ratna experienced.

Outcome and Lessons from Pak Santoso’s Case

Effective estate planning for digital assets involves creating a comprehensive inventory, designating beneficiaries, and appointing a digital executor to handle the technicalities. This proactive approach ensures a smooth transfer of ownership, minimizing stress and maximizing the value of the digital estate. The lack of such planning in Pak Santoso’s case led to significant delays, emotional distress for his family, and potential financial losses. This underscores the importance of staying ahead of the curve, particularly in today’s rapidly evolving digital landscape. The lesson? Don’t let your digital legacy become a digital nightmare.

Final Conclusion

So, there you have it: a whirlwind tour through the world of Estate Planning untuk Keluarga. While the process might seem daunting at first, remember that a well-crafted plan isn’t just about avoiding legal battles; it’s about securing your family’s future and leaving behind a legacy of love, not just legal documents. By understanding the legal framework, effectively managing assets, and fostering open communication, you can create a plan that reflects your family’s unique needs and values. Now go forth and conquer your estate! (But maybe consult a professional too, just in case.)

Question Bank

What happens if I die without a will in Indonesia?

Intestacy rules apply, meaning the distribution of your assets will be determined by Indonesian law, which may not align with your wishes.

How often should I review my estate plan?

It’s advisable to review your estate plan at least every 3-5 years, or whenever there’s a significant life change (marriage, divorce, birth, death).

Can I appoint a non-family member as executor?

Absolutely! A trusted friend or professional can be a great choice, especially if family dynamics are complex.

What are digital assets and how are they handled in estate planning?

Digital assets include online accounts, social media profiles, and digital documents. Proper planning is crucial to access and transfer these after death.

{kind=link}