Navigating the world of insurance can feel overwhelming, but proactive planning is key to securing your financial well-being. This Insurance Planning Guide provides a comprehensive overview of various insurance types, helping you assess your individual needs and choose policies that align with your budget and long-term goals. We’ll explore everything from life and health insurance to property protection, equipping you with the knowledge to make informed decisions and safeguard your future.

From understanding personal risk assessments to effectively managing your policies and filing claims, this guide serves as your roadmap to a secure financial future. We’ll delve into the intricacies of different policy types, comparing their advantages and disadvantages to help you find the perfect fit. The importance of regular reviews and adjustments will also be highlighted, ensuring your coverage remains relevant throughout life’s various stages.

Introduction to Insurance Planning

Insurance planning is the process of identifying and assessing your potential risks, and then developing a strategy to mitigate those risks through the purchase of appropriate insurance policies. It’s a crucial aspect of financial planning, providing a safety net against unforeseen events that could otherwise cause significant financial hardship. Effective insurance planning ensures that you and your loved ones are protected from the devastating financial consequences of accidents, illnesses, or other unexpected occurrences.

Insurance planning involves more than just buying insurance; it’s about strategically selecting the right coverage at the right price to meet your specific needs and circumstances. This involves careful consideration of your current financial situation, future goals, and potential risks. A comprehensive plan considers various factors and ensures adequate protection across multiple areas of life.

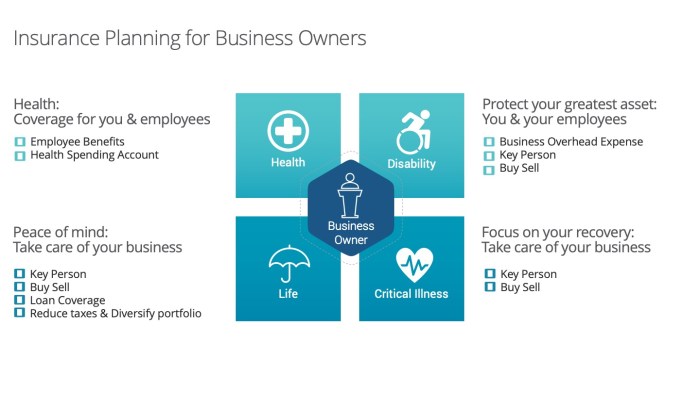

Types of Insurance in a Comprehensive Plan

A well-rounded insurance plan typically includes a variety of coverage types to address different potential risks. Understanding the various types and their functions is essential for creating a truly effective plan.

- Health Insurance: Covers medical expenses, including doctor visits, hospital stays, and prescription drugs. Different plans offer varying levels of coverage and out-of-pocket costs.

- Life Insurance: Provides a financial payout to beneficiaries upon the death of the insured. This payout can help cover funeral expenses, outstanding debts, and provide ongoing financial support for dependents.

- Disability Insurance: Replaces a portion of your income if you become unable to work due to illness or injury. This can help maintain your financial stability during a period of incapacity.

- Homeowners or Renters Insurance: Protects your property and belongings from damage or loss due to events such as fire, theft, or natural disasters. Renters insurance also provides liability coverage.

- Auto Insurance: Covers damages to your vehicle and liability for accidents involving your vehicle. It is typically required by law.

- Long-Term Care Insurance: Helps cover the costs of long-term care services, such as nursing homes or in-home care, which can be extremely expensive.

- Umbrella Insurance: Provides additional liability coverage beyond what is offered by your other policies, offering broader protection against lawsuits.

Key Benefits of Proactive Insurance Planning

Taking a proactive approach to insurance planning offers several significant advantages. Failing to plan can leave you vulnerable to substantial financial burdens during challenging times.

- Financial Security: A well-structured insurance plan provides a crucial safety net, protecting your assets and financial well-being against unexpected events. For example, life insurance can ensure your family’s financial stability after your passing, while disability insurance can prevent financial ruin if you’re unable to work.

- Peace of Mind: Knowing you have adequate insurance coverage can significantly reduce stress and anxiety about the future. This peace of mind allows you to focus on other aspects of your life without the constant worry of financial ruin from unforeseen circumstances.

- Cost Savings: While insurance premiums represent a cost, proactive planning can actually lead to long-term cost savings. Addressing potential risks early can prevent much larger financial losses down the line. For instance, addressing a health issue early through preventative care may avoid far greater expenses related to long-term treatment.

Assessing Individual Needs

Understanding your personal risk profile is crucial for effective insurance planning. A thorough assessment helps determine the appropriate coverage levels to protect yourself and your loved ones from unforeseen financial burdens. This process involves examining various aspects of your life and identifying potential risks that could significantly impact your financial well-being.

A comprehensive personal risk assessment involves several key steps. First, you need to meticulously catalog your assets, including property, investments, and other valuable possessions. Second, you should identify potential liabilities, such as outstanding loans, mortgages, or potential legal responsibilities. Third, you must evaluate potential threats to your assets and income, such as accidents, illness, job loss, or natural disasters. Finally, you should consider your family’s financial needs and dependencies, including dependents, spouses, or elderly parents. This holistic approach ensures a well-rounded understanding of your overall insurance needs.

Factors Influencing Insurance Needs

Several key factors significantly influence an individual’s insurance requirements. These factors interact to shape the type and amount of coverage needed to provide adequate financial protection. Understanding these influences allows for a more personalized and effective insurance plan.

- Age: Insurance needs often change with age. Younger individuals may prioritize health insurance and disability coverage, while older individuals may focus more on long-term care and life insurance to cover estate planning needs. For example, a 25-year-old might focus on health insurance and disability, while a 60-year-old might prioritize long-term care and life insurance to provide for their family or cover funeral expenses.

- Income: Higher income levels often translate to greater assets and higher potential liabilities. This necessitates more comprehensive insurance coverage to protect against significant financial losses. Someone earning a six-figure salary would likely require a higher level of insurance than someone earning minimum wage.

- Family Status: Marital status, number of dependents, and the presence of elderly parents heavily influence insurance needs. For instance, a married couple with young children will require different coverage than a single individual with no dependents. The presence of children necessitates life insurance to provide for their future, while caring for elderly parents might require long-term care insurance.

- Health Status: Pre-existing health conditions or a family history of certain illnesses can significantly impact the need for health insurance and potentially increase premiums. Individuals with pre-existing conditions might need more comprehensive health insurance to cover medical expenses.

- Occupation: High-risk occupations often necessitate specialized insurance coverage. For instance, a construction worker might require additional disability insurance to cover income loss due to work-related injuries, whereas a software engineer might prioritize different types of insurance.

Sample Insurance Needs Questionnaire

A structured questionnaire can help individuals systematically assess their insurance requirements. This self-assessment provides a foundation for a more informed discussion with an insurance professional.

| Question | Response |

|---|---|

| What is your age? | |

| What is your annual income? | |

| What is your marital status? | |

| Do you have any dependents (children, elderly parents)? | |

| Do you own a home or rent? | |

| Do you have any significant debts (mortgages, loans)? | |

| Do you have any pre-existing health conditions? | |

| What is your occupation? | |

| Do you have any valuable assets (investments, jewelry)? | |

| What are your financial goals (retirement, education)? |

Types of Insurance Coverage

Understanding the different types of insurance is crucial for building a comprehensive financial safety net. Choosing the right coverage depends on your individual circumstances, risk tolerance, and financial goals. This section will Artikel some key insurance types and their features.

Insurance policies generally fall into several broad categories, each designed to protect against specific risks. These categories are not mutually exclusive; many individuals will need a combination of policies to adequately protect themselves and their assets.

Life Insurance

Life insurance provides a financial benefit to your beneficiaries upon your death. The payout, called a death benefit, helps cover expenses such as funeral costs, outstanding debts, and ongoing living expenses for your dependents. There are two main types: term life insurance and whole life insurance, each with distinct characteristics.

Term Life Insurance versus Whole Life Insurance

The choice between term and whole life insurance hinges on your needs and financial situation. Both offer death benefits, but they differ significantly in their coverage duration and features.

| Feature | Term Life Insurance | Whole Life Insurance |

|---|---|---|

| Coverage Duration | Specific period (term), e.g., 10, 20, or 30 years | Lifelong coverage, as long as premiums are paid |

| Premiums | Generally lower premiums than whole life | Higher premiums than term life |

| Cash Value | No cash value accumulation | Builds cash value that can be borrowed against or withdrawn |

| Advantages | Affordable, provides coverage for a specific period when needed most (e.g., raising children) | Lifetime coverage, cash value accumulation offers potential financial benefits |

| Disadvantages | Coverage expires at the end of the term; no cash value | Higher premiums, may not be the most cost-effective option for younger individuals |

Health Insurance

Health insurance covers medical expenses, including doctor visits, hospital stays, surgeries, and prescription drugs. The specific coverage varies depending on the policy and plan chosen. Health insurance can significantly reduce the financial burden of unexpected medical costs. Choosing a plan with appropriate coverage is crucial for managing healthcare expenses effectively. Different plans offer various levels of coverage and cost-sharing mechanisms such as deductibles and co-pays.

Disability Insurance

Disability insurance provides income replacement if you become unable to work due to illness or injury. This crucial coverage protects your financial stability during a period when you may be unable to earn a living. The benefits typically replace a portion of your income, helping you meet your financial obligations while recovering. Different policies offer varying levels of benefit amounts and waiting periods before benefits begin.

Property Insurance

Property insurance protects your assets from damage or loss due to unforeseen events such as fire, theft, or natural disasters. This can include homeowner’s insurance, renter’s insurance, or commercial property insurance, depending on the type of property being insured. These policies typically cover the cost of repairing or replacing damaged property and may also cover liability for accidents that occur on your property.

The Importance of Riders and Add-ons

Riders and add-ons are optional provisions that can enhance the coverage of your insurance policy. They provide additional protection or benefits beyond the standard policy features. Carefully considering available riders and add-ons can significantly improve the overall value and effectiveness of your insurance plan.

For example, a life insurance policy might offer a waiver of premium rider, which would continue coverage even if the policyholder becomes disabled and unable to pay premiums. A long-term care rider can add coverage for long-term care expenses. These are just a few examples; the availability of riders and add-ons varies greatly depending on the insurer and the type of policy.

Choosing the Right Policy

Selecting the right insurance policy can feel overwhelming, but a systematic approach simplifies the process. By carefully considering your individual needs and budget, you can find a policy that provides adequate protection without unnecessary expense. This section will guide you through the steps involved in choosing the best insurance for your circumstances.

Step-by-Step Policy Selection

Choosing the right insurance policy involves several key steps. First, accurately assess your needs. What risks are you most concerned about? How much coverage do you require to mitigate those risks? Next, establish a realistic budget. How much can you comfortably afford to pay in premiums each month or year? Once you have a clear understanding of your needs and budget, you can begin researching different policies and comparing quotes. Finally, carefully review the policy details before making a final decision, paying close attention to exclusions and limitations.

Comparing Insurance Quotes

When comparing insurance quotes from different providers, several crucial factors should be considered. Premium costs are obviously important, but equally important are the levels of coverage offered. Examine the policy’s terms and conditions meticulously, paying particular attention to deductibles, co-pays, and out-of-pocket maximums. Consider the provider’s reputation and financial stability. Check independent ratings and reviews to gauge their reliability and customer service quality. Don’t solely focus on the lowest price; a slightly more expensive policy might offer significantly better coverage and benefits in the long run. Also, consider the ease of filing claims and the provider’s responsiveness to customer inquiries.

Health Insurance Plan Comparison

The following table compares key features of three common types of health insurance plans: High Deductible Health Plan (HDHP), Preferred Provider Organization (PPO), and Health Maintenance Organization (HMO). Remember that specific benefits and costs vary widely depending on the provider and your location. This table provides a general overview for illustrative purposes.

| Feature | High Deductible Health Plan (HDHP) | Preferred Provider Organization (PPO) | Health Maintenance Organization (HMO) |

|---|---|---|---|

| Monthly Premium | Generally Low | Moderate | Generally Low |

| Annual Deductible | High | Moderate | Low to Moderate |

| Out-of-Pocket Maximum | High | High | Moderate |

| Network Restrictions | Generally Fewer Restrictions | Fewer Restrictions than HMOs | Strict Network Restrictions |

| Doctor Choice | More Choice | More Choice than HMOs | Limited Choice; Must choose from network |

| Referral Requirements | Generally No Referrals Needed | Generally No Referrals Needed | Referrals Often Required |

Managing and Reviewing Insurance Policies

Effective insurance planning isn’t a one-time event; it’s an ongoing process requiring diligent management and regular review. Maintaining organized records and proactively assessing your coverage ensures you’re adequately protected and can efficiently handle any claims. This section will guide you through best practices for managing your insurance policies and navigating the claims process.

Organizing and accessing your insurance information efficiently is crucial for peace of mind and effective claims management. A well-organized system prevents unnecessary stress during unexpected events.

Efficiently Managing Insurance Documents

Creating a central repository for all your insurance documents is the first step toward effective management. This could be a dedicated physical file, a secure digital folder on your computer, or a cloud-based storage system. Regardless of your chosen method, ensure your system is easily accessible and well-organized. Consider using a system of labeled folders or subfolders to categorize your policies by type (e.g., auto, home, health) or insurer. Maintain digital copies of all documents, ideally in PDF format, to prevent loss or damage. Additionally, keep a physical copy of essential documents in a secure, fireproof location. Remember to update your information whenever there are changes in your policy or personal circumstances.

Regular Policy Reviews and Adjustments

Regular review of your insurance policies is vital to ensure they still meet your needs. Life circumstances change – marriage, childbirth, new home purchase, career changes – all of which can impact your insurance requirements. Annual reviews are recommended, allowing you to assess whether your coverage amounts are still appropriate, your deductibles are manageable, and your policy terms remain favorable. This process also helps identify potential gaps in coverage that could leave you vulnerable to financial loss. For instance, if you recently purchased a new home, you may need to increase your homeowner’s insurance coverage to reflect the increased value of your property. Similarly, a career change might necessitate reviewing your disability insurance coverage.

Filing an Insurance Claim

Filing a claim can be daunting, but a systematic approach can streamline the process. Begin by promptly notifying your insurance company of the incident. This initial notification typically involves contacting them by phone or through their online portal. Following this initial contact, gather all necessary documentation to support your claim. This typically includes proof of loss (police report for theft, medical records for health insurance), photos or videos of the damage, and any relevant contracts or receipts. Complete the claim form accurately and thoroughly, providing all requested information. Keep copies of all submitted documents for your records. Maintain open communication with your insurance adjuster throughout the claims process, promptly responding to any requests for additional information. Be patient, as the claims process can take time depending on the complexity of the claim and the insurer’s procedures. Remember to carefully review the settlement offer before accepting it to ensure it fairly compensates you for your losses.

Long-Term Financial Planning and Insurance

Securing your financial future requires a comprehensive strategy that extends beyond immediate needs. Long-term financial planning encompasses a broad range of goals, from comfortable retirement to a well-defined estate plan. Insurance plays a vital, often underestimated, role in mitigating risks and safeguarding these long-term aspirations. By strategically integrating insurance into your overall financial plan, you can build a resilient foundation capable of weathering unforeseen events and ensuring the achievement of your financial objectives.

Insurance acts as a crucial safety net in long-term financial planning, protecting against events that could severely impact your financial stability. Unexpected illnesses, disabilities, or even premature death can derail carefully constructed retirement plans or leave heirs with significant financial burdens. The right insurance coverage acts as a buffer against these risks, allowing you to maintain financial stability and continue progressing toward your goals even in the face of adversity. This protection extends to both personal and business assets, ensuring the continuity of your legacy and the well-being of your loved ones.

Retirement Planning and Insurance

Retirement planning often focuses on accumulating sufficient assets to support a comfortable lifestyle after ceasing employment. However, unforeseen circumstances can significantly impact these plans. Long-term care insurance, for instance, can protect against the potentially crippling costs associated with extended nursing home stays or in-home care. Life insurance, particularly a policy with a substantial death benefit, can provide a financial safety net for surviving family members, ensuring they can maintain their lifestyle and meet financial obligations. Annuities can provide a guaranteed stream of income during retirement, mitigating the risk of outliving your savings. These insurance products work in concert with retirement savings accounts (like 401(k)s and IRAs) to provide a comprehensive and secure retirement strategy. For example, a couple nearing retirement could utilize a combination of a 401(k) for regular income, a life insurance policy to protect their spouse upon death, and a long-term care policy to cover potential healthcare expenses.

Estate Planning and Insurance

Estate planning involves the management and distribution of your assets after your death. Life insurance plays a key role in ensuring a smooth and efficient transfer of wealth. A life insurance policy with a designated beneficiary can provide the funds necessary to pay estate taxes, cover funeral expenses, and provide for the financial needs of surviving family members. This ensures that your estate is properly managed and distributed according to your wishes, minimizing potential disputes and financial hardship for your loved ones. Furthermore, insurance can protect against liability claims that could deplete the estate’s value. For instance, an umbrella liability policy could cover significant legal and financial liabilities that might arise after your death. This protects the inheritance for your beneficiaries.

Insurance Integration with Other Financial Tools

Effective long-term financial planning necessitates the integration of various financial tools. Insurance should not be considered in isolation but rather as a crucial component of a holistic strategy. Insurance works synergistically with investment strategies, providing a safety net while your investments grow. For example, a well-diversified investment portfolio complemented by adequate insurance coverage minimizes the impact of market fluctuations and unforeseen events. Similarly, insurance should be integrated with estate planning documents, such as wills and trusts, to ensure the efficient and equitable distribution of assets. A comprehensive estate plan that incorporates life insurance, long-term care insurance, and other insurance products will effectively protect your assets and secure the financial future of your loved ones. A well-structured will, for example, can clearly Artikel the allocation of life insurance proceeds, ensuring the funds are used as intended.

Illustrative Examples

Understanding insurance can be challenging, but seeing how it works in practice clarifies its value. The following scenarios illustrate how different insurance plans can address various life stages and significant life events. Each example highlights specific needs and how the chosen insurance plan helps mitigate potential financial risks.

Scenario 1: Newly Married Couple Purchasing a Home

This scenario depicts a young couple, Sarah and Mark, who recently got married and are buying their first home. Their primary concerns revolve around protecting their new asset and securing their financial future together.

- Insurance Needs: Mortgage protection insurance, homeowner’s insurance, life insurance (potentially with a term life policy for affordability), and health insurance.

- Chosen Plan: They opt for a 20-year term life insurance policy with a death benefit sufficient to cover their mortgage and other debts. They also purchase a comprehensive homeowner’s insurance policy that covers damage from fire, theft, and other unforeseen events. They choose a health insurance plan with a reasonable deductible to protect against medical expenses. They explore mortgage protection insurance to ensure their mortgage is covered in case of death or disability of either spouse.

- How the Plan Addresses Needs: The term life insurance policy provides financial security for Sarah if Mark were to pass away, ensuring the mortgage is paid off. The homeowner’s insurance protects their investment in their home. Health insurance provides financial protection against unexpected medical costs, preventing financial strain from illness or injury. The mortgage protection insurance offers additional security by paying off the mortgage if one of them is unable to work due to disability.

Scenario 2: Expecting Parents

This scenario focuses on Emily and David, who are expecting their first child. Their priorities shift towards protecting their growing family and covering the significant costs associated with raising a child.

- Insurance Needs: Increased life insurance coverage, disability insurance, health insurance with comprehensive maternity coverage, and potentially critical illness insurance.

- Chosen Plan: They increase their life insurance coverage to ensure sufficient funds to support their child if either parent passes away. They consider a disability income insurance policy to replace lost income if one parent becomes unable to work. They ensure their health insurance plan offers comprehensive maternity coverage to cover prenatal care, delivery, and postnatal care. They also explore the possibility of critical illness insurance to cover costs associated with serious illnesses.

- How the Plan Addresses Needs: The increased life insurance coverage provides financial security for their child. Disability insurance replaces income lost due to illness or injury, ensuring the family can maintain their lifestyle. Comprehensive maternity coverage covers the significant costs associated with childbirth, preventing substantial out-of-pocket expenses. Critical illness insurance can provide financial support during difficult times associated with a serious illness.

Scenario 3: Retirement Planning

This scenario highlights the insurance needs of a couple, John and Mary, nearing retirement. Their focus is on securing their financial future and protecting their assets during their retirement years.

- Insurance Needs: Long-term care insurance, supplemental health insurance (Medicare Supplement), and possibly an annuity to provide a guaranteed income stream.

- Chosen Plan: They purchase a long-term care insurance policy to help cover the costs of long-term care services should they need assistance with daily living activities. They also acquire a Medicare Supplement plan to help cover out-of-pocket expenses associated with Medicare. They explore purchasing an annuity to provide a steady stream of income during retirement.

- How the Plan Addresses Needs: Long-term care insurance protects their savings from being depleted by the high cost of long-term care. The Medicare Supplement plan reduces out-of-pocket expenses associated with healthcare in retirement. The annuity provides a guaranteed income stream, offering financial security and peace of mind during their retirement years.

Epilogue

Ultimately, effective insurance planning is about more than just protection; it’s about peace of mind. By understanding your risks, selecting appropriate coverage, and regularly reviewing your policies, you can confidently navigate life’s uncertainties and focus on achieving your long-term financial aspirations. This guide provides the foundation for a secure future, empowering you to take control of your financial well-being and protect what matters most.

Helpful Answers

What is the difference between term and whole life insurance?

Term life insurance provides coverage for a specific period, offering lower premiums but no cash value. Whole life insurance offers lifelong coverage with a cash value component that grows over time, but premiums are generally higher.

How often should I review my insurance policies?

It’s recommended to review your insurance policies at least annually, or whenever there’s a significant life change (marriage, birth of a child, job change, etc.).

What documents do I need to file an insurance claim?

Required documents vary depending on the type of claim, but generally include the policy details, a claim form, and supporting documentation related to the incident (e.g., police report, medical records).

Can I change my insurance policy after it’s been issued?

Yes, you can often make changes to your policy, such as increasing or decreasing coverage, adding riders, or changing payment options. However, there may be limitations depending on the policy type and insurer.

{kind=link}