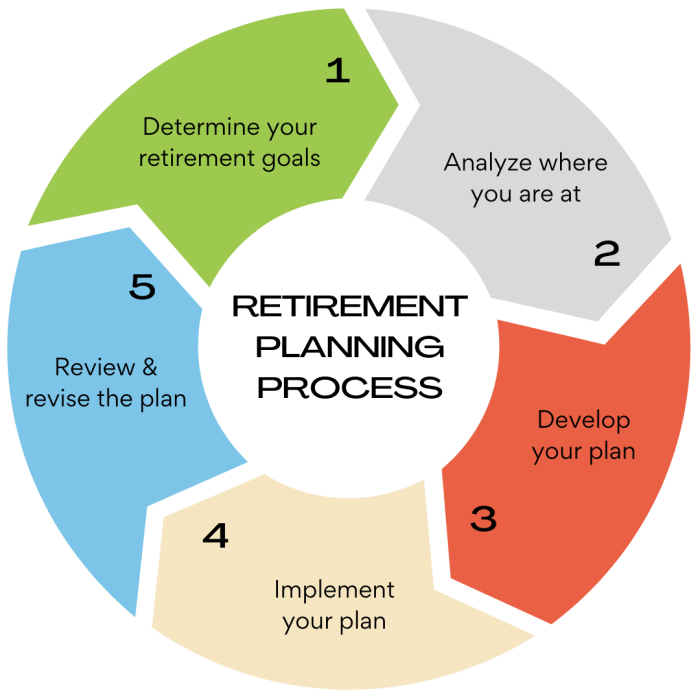

Retirement Planning Guide: Secure Your Future. This guide navigates the complexities of securing a comfortable retirement, offering a comprehensive roadmap to financial independence. We’ll explore setting realistic goals, assessing your current financial health, and developing a robust strategy to manage income and expenses throughout your golden years. From understanding various retirement accounts and investment options to navigating healthcare costs and estate planning, this guide equips you with the knowledge and tools to confidently plan for your future.

This guide provides a step-by-step approach, addressing key aspects such as defining retirement goals aligned with your lifestyle, assessing your current financial standing, planning for diverse income streams, managing potential expenses, and ensuring a smooth transition into retirement. We’ll also delve into crucial considerations like estate planning, healthcare, and the tax implications of your retirement strategy. Through illustrative examples and practical tools, we aim to empower you to take control of your retirement planning journey.

Defining Retirement Goals

Planning for retirement involves envisioning your ideal lifestyle and translating that vision into concrete financial goals. This requires careful consideration of your spending habits, desired activities, and potential healthcare costs. Understanding your retirement income needs is crucial for ensuring a comfortable and fulfilling retirement.

Retirement Lifestyle Scenarios and Associated Costs

Different retirement lifestyles demand varying levels of financial resources. A minimalist lifestyle, focused on essential needs and limited leisure activities, will have significantly lower costs than a lavish lifestyle involving extensive travel, luxury goods, and frequent dining out. Consider these examples:

- Minimalist Lifestyle: This lifestyle prioritizes essential expenses like housing, groceries, utilities, and healthcare. It involves limited travel and entertainment. Estimated monthly costs could range from $2,000 to $4,000, depending on location and individual needs.

- Moderate Lifestyle: This involves a balance between essential expenses and some discretionary spending, such as occasional travel, dining out, and hobbies. Estimated monthly costs might range from $4,000 to $8,000, depending on location and choices.

- Lavish Lifestyle: This lifestyle prioritizes luxury goods, frequent travel, expensive hobbies, and high-end entertainment. Monthly costs could easily exceed $8,000 and vary greatly depending on individual preferences.

These are just examples, and individual costs will vary greatly based on factors such as location, health status, and personal preferences. It’s important to consider inflation and potential unexpected expenses when estimating retirement costs.

Retirement Income Needs Assessment Worksheet

This worksheet helps you estimate your annual retirement income needs.

| Category | Estimated Monthly Cost | Estimated Annual Cost |

|---|---|---|

| Housing (rent/mortgage, property taxes, insurance) | ||

| Food | ||

| Utilities (electricity, water, gas) | ||

| Transportation (car payments, gas, insurance, public transport) | ||

| Healthcare (insurance premiums, medical expenses) | ||

| Entertainment and Leisure | ||

| Travel | ||

| Clothing | ||

| Personal Care | ||

| Other Expenses | ||

| Total Monthly Expenses | ||

| Total Annual Expenses |

To complete this worksheet, fill in your estimated monthly costs for each category. Then, multiply your total monthly expenses by 12 to determine your estimated annual retirement income needs. Remember to adjust for inflation. For example, using a conservative inflation rate of 3% annually, your expenses will likely increase over time.

Realistic Retirement Goals for Various Age Groups and Income Levels

Retirement goals vary greatly depending on age, current income, and savings. A 35-year-old with a high income might aim for early retirement with a significant nest egg, while a 55-year-old with a moderate income might focus on maintaining their current lifestyle.

- 30-40 Year Olds (High Income): May aim for early retirement (age 55-60) with a substantial investment portfolio and passive income streams, potentially requiring millions in savings.

- 30-40 Year Olds (Moderate Income): May aim for a comfortable retirement around the traditional retirement age (65-67), requiring diligent saving and investment strategies.

- 50-60 Year Olds (Moderate Income): May focus on maximizing existing savings and investments to maintain their current lifestyle in retirement, potentially requiring adjustments to spending habits.

- 50-60 Year Olds (Low Income): May need to rely heavily on Social Security and potentially part-time work to supplement their income in retirement.

These are just examples, and individual circumstances will vary significantly. It’s crucial to create a personalized retirement plan that aligns with your individual goals and financial situation. Seeking professional financial advice is recommended to create a comprehensive and realistic retirement plan.

Assessing Current Financial Situation

Understanding your current financial standing is crucial for effective retirement planning. A clear picture of your assets and liabilities allows you to realistically assess your progress toward your retirement goals and make informed decisions about your savings and investment strategies. This involves creating a personal balance sheet and evaluating your savings and investments.

Creating a Personal Balance Sheet to Understand Net Worth

A personal balance sheet is a snapshot of your financial health at a specific point in time. It lists your assets (what you own) and liabilities (what you owe), and the difference between the two represents your net worth. A positive net worth indicates you have more assets than liabilities, while a negative net worth signifies the opposite. Regularly updating your balance sheet provides valuable insights into your financial progress and helps you track your net worth over time. This information is vital for setting realistic retirement goals and making informed financial decisions. For example, someone with a high net worth might be able to retire earlier than someone with a lower net worth, assuming all other factors are equal.

Calculating Current Savings and Investment Portfolio Value

Accurately determining the value of your savings and investments is essential for assessing your financial readiness for retirement. This involves gathering information from various sources, including bank statements, brokerage account statements, and retirement account statements. For savings accounts, the value is simply the current balance. For investment accounts, you need to consider the current market value of your holdings, which may fluctuate daily. You should consult your brokerage statements or online account portals for the most up-to-date figures. It’s important to be thorough and include all relevant accounts, such as checking and savings accounts, investment accounts (stocks, bonds, mutual funds), and retirement accounts. For example, a person might have $50,000 in a savings account, $100,000 in a brokerage account, and $75,000 in a 401(k) for a total investment portfolio value of $225,000.

Comparing Different Types of Retirement Accounts

Different retirement accounts offer varying benefits and tax advantages. Understanding these differences is critical for maximizing your retirement savings.

| Account Type | Contribution Limits (2023) | Tax Advantages | Withdrawal Rules |

|---|---|---|---|

| 401(k) | $22,500 (plus $7,500 catch-up for age 50+) | Contributions typically pre-tax; earnings grow tax-deferred. | Taxes owed on withdrawals in retirement. Early withdrawals may incur penalties. |

| Traditional IRA | $6,500 (plus $1,000 catch-up for age 50+) | Contributions may be tax-deductible; earnings grow tax-deferred. | Taxes owed on withdrawals in retirement. Early withdrawals may incur penalties. |

| Roth IRA | $6,500 (plus $1,000 catch-up for age 50+) | Contributions are not tax-deductible; earnings grow tax-free. | Tax-free withdrawals in retirement, provided certain conditions are met. Early withdrawals of contributions are tax-free and penalty-free. |

Planning for Retirement Income

Securing a comfortable retirement requires careful planning and a comprehensive understanding of your potential income sources. This section will explore the various avenues for generating retirement income, discuss different investment strategies, and provide a practical guide for estimating your total retirement income. Understanding these elements is crucial for achieving your desired lifestyle in retirement.

Sources of Retirement Income

Retirement income typically comes from a combination of sources. Relying solely on one source is generally risky; diversification is key to mitigating potential shortfalls. The primary sources include Social Security benefits, pensions (if applicable), and personal savings and investments. Each source has its own characteristics and limitations, which need to be considered in your overall retirement plan.

- Social Security: Social Security provides a baseline level of income for many retirees. The amount received depends on your earnings history and the age at which you begin receiving benefits. Delaying benefits can result in a higher monthly payment, but you will receive fewer overall payments. It’s advisable to consult the Social Security Administration’s website for personalized benefit estimates.

- Pensions: Defined benefit pensions, if available through your employer, provide a guaranteed monthly income stream throughout retirement. The amount is typically based on your salary and years of service. However, defined benefit pensions are becoming less common.

- Personal Savings and Investments: This encompasses a wide range of assets, including retirement accounts (401(k)s, IRAs), taxable brokerage accounts, and other investments. The income generated from these assets will depend on the investment strategy employed and market performance.

Investment Strategies for Retirement

Investment strategies for retirement should align with your risk tolerance, time horizon, and retirement goals. Generally, a longer time horizon allows for a higher risk tolerance, as there’s more time to recover from potential market downturns.

- Low-Risk Investments: These investments prioritize capital preservation over high growth. Examples include certificates of deposit (CDs), government bonds, and money market accounts. They offer lower returns but provide stability and minimize the risk of losing principal.

- High-Risk Investments: These investments aim for higher returns but carry a greater risk of loss. Examples include stocks, particularly individual stocks, and some types of real estate. While potentially offering significant growth, these investments are subject to market fluctuations.

- Diversified Portfolio: A balanced approach typically involves diversifying across different asset classes to mitigate risk. A portfolio might include a mix of stocks, bonds, and real estate, with the allocation adjusted based on individual circumstances and risk tolerance.

Calculating Estimated Retirement Income

Accurately estimating your retirement income requires a systematic approach. This involves projecting income from each source and summing them to obtain a total estimated income.

- Estimate Social Security benefits: Use the Social Security Administration’s online retirement estimator to get a personalized estimate based on your earnings history and planned retirement age.

- Estimate pension income: If you have a defined benefit pension, your employer should provide information on your projected monthly payment.

- Estimate income from savings and investments: This is more complex and requires making assumptions about investment returns. You can use a retirement calculator or work with a financial advisor to model different scenarios and estimate potential income based on various withdrawal rates (e.g., 4% rule).

- Sum the estimates: Add the estimated income from each source (Social Security, pension, and investments) to arrive at your total estimated retirement income.

Example: Let’s say John estimates $2,000 monthly from Social Security, $1,500 from his pension, and $3,000 from his investments. His total estimated monthly retirement income would be $6,500.

Managing Retirement Expenses

Retirement, while a time for relaxation and pursuing passions, also requires careful financial planning to ensure a comfortable lifestyle. Understanding and managing your expenses is crucial to achieving your retirement goals and avoiding financial stress. This section will explore potential unexpected costs, common expense categories, and provide a budgeting template to help you navigate this important aspect of retirement planning.

Potential Unexpected Expenses During Retirement

Unexpected expenses can significantly impact your retirement budget. These can range from minor home repairs to major medical emergencies. Failing to account for these possibilities can lead to financial hardship. It’s crucial to proactively plan for unforeseen circumstances.

- Home Repairs and Maintenance: As homes age, they require increasing maintenance and repairs. Roof replacements, plumbing issues, and appliance malfunctions can be costly.

- Unexpected Medical Expenses: Even with health insurance, unexpected medical bills can arise. These might include unexpected surgeries, long-term care needs, or prescription drug costs.

- Vehicle Repairs and Replacement: Car maintenance and eventual replacement are significant expenses. Factor in potential repairs, insurance, and the cost of a new vehicle.

- Long-Term Care: The need for assisted living or in-home care can be a substantial expense, especially if it’s not adequately covered by insurance.

- Inflation: The rising cost of goods and services over time erodes purchasing power. Building in a buffer for inflation is essential.

Typical Retirement Expenses

Retirement expenses can be categorized into several key areas: housing, healthcare, and leisure activities. Understanding the typical costs in each area is crucial for accurate budget planning.

Housing Costs

Housing typically represents a significant portion of retirement expenses. These costs can vary widely depending on location, homeownership status, and lifestyle choices. Consider mortgage payments (if applicable), property taxes, homeowners insurance, utilities, and potential home maintenance and repairs. For example, a retiree living in a high-cost area might face significantly higher housing costs compared to someone in a more affordable region. Downsizing to a smaller home or relocating to a less expensive area can significantly reduce these expenses.

Healthcare Costs

Healthcare is another major expense during retirement. Even with Medicare, out-of-pocket costs for premiums, deductibles, co-pays, and prescription drugs can be substantial. Consider the potential need for long-term care, which can be exceptionally expensive. For instance, a retiree with pre-existing health conditions might face higher medical expenses than a healthy individual. Exploring supplemental health insurance options can help mitigate these costs.

Leisure Activities

While retirement offers time for leisure activities, these can also add to your expenses. Travel, hobbies, entertainment, and dining out all contribute to your overall budget. For example, a retiree who enjoys extensive travel might need to allocate a larger portion of their budget to this category than someone who prefers more sedentary activities. Careful planning and prioritizing can help manage these costs effectively.

Retirement Budget Template

| Expense Category | Monthly Budget | Annual Budget |

|---|---|---|

| Housing | ||

| Healthcare (Premiums, Co-pays, Medications) | ||

| Food | ||

| Transportation | ||

| Utilities | ||

| Insurance (Home, Auto, Health Supplements) | ||

| Personal Care | ||

| Leisure Activities | ||

| Savings & Investments | ||

| Debt Payments | ||

| Total Monthly Expenses | ||

| Total Annual Expenses |

Remember to regularly review and adjust your budget as needed to account for changing circumstances and inflation.

Estate Planning and Legacy

Planning for your estate isn’t just about what happens to your assets after you’re gone; it’s about securing your family’s future and leaving a legacy that reflects your values. A well-structured estate plan provides peace of mind, knowing your wishes will be carried out, and minimizes potential conflict and financial burdens for your loved ones. This section Artikels key elements of estate planning and offers strategies to consider.

Creating a Will and Establishing a Power of Attorney

A will is a legal document that dictates how your assets will be distributed after your death. Without a will, your assets will be distributed according to your state’s intestacy laws, which may not align with your wishes. Establishing a power of attorney designates someone to manage your financial and/or healthcare affairs if you become incapacitated. This ensures your affairs are handled responsibly even if you are unable to manage them yourself. Both a will and a power of attorney are crucial components of a comprehensive estate plan, offering control and protection. A properly drafted will clearly specifies beneficiaries for assets, appoints an executor to manage the estate, and may include instructions regarding guardianship of minor children. Similarly, a power of attorney designates an agent to act on your behalf, with varying degrees of authority specified in the document.

Steps Involved in Creating a Comprehensive Estate Plan

Developing a comprehensive estate plan is a multi-step process requiring careful consideration and, ideally, professional guidance. First, you need to inventory all your assets, including real estate, investments, bank accounts, and personal property. Next, identify your beneficiaries – the individuals or entities who will inherit your assets. Then, you’ll need to decide how you want your assets distributed. This involves determining the percentages or specific assets each beneficiary will receive. The next step is to select an executor for your will, who will be responsible for carrying out your wishes. Finally, you’ll need to consult with an estate planning attorney to draft and execute your legal documents, ensuring they are legally sound and reflect your intentions accurately. This process ensures a smooth transition of assets and minimizes potential legal disputes.

Estate Planning Strategies for Various Family Structures and Asset Levels

Estate planning strategies vary depending on individual circumstances, such as family structure and asset levels. For example, a couple with minor children might establish trusts to protect their children’s inheritance until they reach adulthood. High-net-worth individuals may employ more complex strategies, such as creating irrevocable trusts to minimize estate taxes. Families with blended families may require careful consideration of how assets are distributed to ensure fairness and prevent potential conflict among family members. Individuals with modest assets might opt for simpler wills and power of attorney documents. It’s crucial to tailor your estate plan to your specific needs and circumstances, seeking professional advice when necessary to navigate the complexities of estate law. For instance, a family with significant real estate holdings might utilize a trust to facilitate the transfer of property to heirs while minimizing tax implications, whereas a family with primarily liquid assets might focus on straightforward beneficiary designations on accounts.

Healthcare Considerations in Retirement

Planning for healthcare costs is a crucial aspect of retirement preparation. Unexpected medical expenses can significantly impact your retirement budget, so understanding your options and making proactive plans is essential for maintaining financial security and peace of mind during your golden years. This section will Artikel key considerations regarding healthcare in retirement.

Medicare and Supplemental Insurance

Medicare is the primary health insurance program for individuals aged 65 and older and certain younger people with disabilities. It’s a federal program with several parts: Part A (hospital insurance), Part B (medical insurance), Part C (Medicare Advantage plans offered by private companies), and Part D (prescription drug insurance). Each part has its own costs and coverage details. Understanding these nuances is vital for choosing the best plan for your individual needs. Many retirees opt for supplemental insurance, also known as Medigap, to cover the gaps in Medicare coverage, such as co-pays, deductibles, and other out-of-pocket expenses. Medigap policies are offered by private insurance companies and vary in coverage and cost. Carefully comparing plans from different providers is crucial to finding the most suitable and affordable option.

Long-Term Care Costs and Management Strategies

Long-term care, which can include nursing home care, assisted living, or in-home care, can be incredibly expensive. The average annual cost of a nursing home varies significantly by location but can easily exceed $100,000. Planning for these potential costs is critical. Strategies for managing these expenses include purchasing long-term care insurance, which provides financial assistance for long-term care services, or setting aside funds in a dedicated savings account. Another option involves exploring government assistance programs, such as Medicaid, which may cover long-term care for individuals who meet specific income and asset requirements. For example, a couple planning for retirement might allocate a specific portion of their savings to a long-term care fund, possibly supplemented by a long-term care insurance policy to mitigate the financial risk.

Healthcare-Related Documents and Preparations

Preparing essential healthcare documents before retirement is crucial for ensuring smooth access to care and facilitating decision-making in case of unforeseen circumstances. This includes having an updated advance directive, which Artikels your wishes regarding medical treatment if you become incapacitated. This often includes a living will specifying your preferences for life-sustaining treatment and a durable power of attorney for healthcare, designating someone to make healthcare decisions on your behalf. Additionally, maintaining a comprehensive list of your doctors, medications, allergies, and insurance information is vital for efficient healthcare management. A well-organized medical record binder, accessible to both yourself and your designated healthcare proxy, is a highly recommended practice. Finally, it is important to review your insurance coverage regularly and update it as your health needs change.

Tax Implications of Retirement Planning

Retirement planning involves careful consideration of the tax implications of various savings and withdrawal strategies. Understanding these implications is crucial for maximizing your retirement income and minimizing your tax burden throughout your retirement years. Failing to account for taxes can significantly reduce the actual amount of money available to you in retirement.

Tax Implications of Different Retirement Accounts

Different retirement accounts offer varying levels of tax advantages. Traditional IRAs and 401(k)s allow for pre-tax contributions, reducing your taxable income in the present. However, withdrawals in retirement are taxed as ordinary income. Roth IRAs, conversely, involve after-tax contributions, but withdrawals in retirement are generally tax-free. This difference significantly impacts your overall tax liability throughout your life. For example, a high-income earner might find a Roth IRA more beneficial in the long run, despite the immediate higher tax burden, while someone in a lower tax bracket might prefer the immediate tax benefits of a traditional IRA. Employer-sponsored plans often offer a combination of pre-tax and Roth options, allowing for tailored strategies based on individual circumstances and projections.

Tax-Efficient Retirement Planning Strategies

Several strategies can help minimize your tax liability during retirement. Tax-loss harvesting, for instance, involves selling investments that have lost value to offset capital gains taxes on other investments. This strategy can be particularly useful in managing taxes during retirement when you might be required to withdraw money from tax-deferred accounts. Diversifying your investments across different asset classes can also help manage tax exposure. For example, combining tax-advantaged accounts with taxable brokerage accounts allows for a more flexible approach to managing withdrawals and capital gains. Careful consideration of the tax implications of each investment decision is essential. An example might involve choosing municipal bonds for their tax-exempt interest, which can significantly reduce your overall tax burden compared to taxable corporate bonds.

Tax Implications of Withdrawal Strategies

The timing and type of withdrawals from retirement accounts have significant tax implications. Withdrawing from a traditional IRA or 401(k) results in ordinary income tax on the withdrawn amount. However, Roth IRA withdrawals are generally tax-free, provided the withdrawal is made after the five-year period and meets certain requirements. Required Minimum Distributions (RMDs) from traditional accounts begin at age 73 (or 75, depending on the year of birth) and are subject to income tax. Failing to take RMDs can result in substantial penalties. The age at which you start withdrawing money significantly impacts your tax liability. For instance, withdrawing a large sum early in retirement could push you into a higher tax bracket, reducing your after-tax income.

Flowchart Illustrating Tax Implications of Withdrawals

[Imagine a flowchart here. The flowchart would depict different retirement accounts (Traditional IRA, Roth IRA, 401(k)) branching out to different age ranges (before 73/75, after 73/75). Each branch would then lead to a box indicating the tax implications (taxed as ordinary income, tax-free, subject to RMDs and ordinary income tax). Arrows would indicate the flow of decisions and their consequences. The flowchart would visually represent the complexities of tax implications at different life stages and account types.]

Adjusting Your Plan

Retirement planning isn’t a set-it-and-forget-it endeavor. Life throws curveballs, and your financial strategy needs to be flexible enough to adapt to unexpected events and changing circumstances. Regularly reviewing and adjusting your plan is crucial to ensuring you stay on track toward your retirement goals.

Unexpected life events, such as job loss or serious health issues, can significantly impact your retirement savings and timeline. Similarly, economic shifts, including inflation or market downturns, necessitate adjustments to maintain your financial security. Proactive planning and adaptation are key to navigating these challenges and preserving your retirement prospects.

Adapting to Unexpected Life Events

Job loss or a significant reduction in income can severely disrupt retirement savings. Strategies for mitigating this include immediately reviewing your budget to identify areas for cost reduction, exploring alternative income sources (part-time work, consulting), and potentially delaying retirement. If health issues arise, consider the potential impact on healthcare costs and long-term care needs. Adjusting your retirement plan might involve increasing your health savings account contributions, purchasing long-term care insurance, or exploring options for in-home care to minimize future expenses. For example, if a sudden illness necessitates a significant increase in medical expenses, you might need to withdraw a portion of your retirement savings to cover the costs, potentially impacting your overall retirement fund. This underscores the importance of having emergency funds readily available and reviewing your insurance coverage regularly.

Responding to Changing Economic Conditions

Economic downturns can significantly impact retirement portfolios. During periods of high inflation, the purchasing power of your savings diminishes. Strategies to address this include diversifying your investment portfolio to mitigate risk, adjusting your investment strategy to align with market conditions, and considering delaying withdrawals if market performance is poor. For instance, during a period of high inflation, you might shift a greater portion of your investments into assets that historically perform well during inflationary periods, such as real estate or inflation-protected securities. Conversely, if the market experiences a downturn, you may choose to delay withdrawals or reduce the amount you withdraw to protect your principal.

Resources for Professional Financial Advice

Seeking professional guidance is often beneficial, especially during times of uncertainty. A certified financial planner (CFP) can provide personalized advice based on your individual circumstances and goals.

- Certified Financial Planner Board of Standards Inc. (CFP Board): This organization provides a directory of CFP professionals.

- National Association of Personal Financial Advisors (NAPFA): NAPFA offers a directory of fee-only financial advisors.

- Financial Industry Regulatory Authority (FINRA): FINRA’s BrokerCheck tool allows you to check the background of brokers and investment advisors.

Remember, seeking professional advice is a proactive step towards securing a comfortable retirement. Regularly reviewing your plan and adapting to life’s changes will increase the likelihood of achieving your financial goals.

Illustrative Example: Sarah’s Retirement Plan

This example follows Sarah, a 35-year-old marketing professional, as she navigates the process of retirement planning. Her journey highlights common challenges and effective strategies for building a secure financial future. We will track her progress over time, illustrating how her plan adapts to changing circumstances and life events.

Sarah’s primary goal is to retire comfortably at age 65, maintaining her current lifestyle and having enough funds for travel and leisure activities. She understands that achieving this requires careful planning and consistent effort. She also aims to leave a legacy for her family.

Sarah’s Initial Assessment and Goal Setting

At age 35, Sarah begins her retirement planning journey by assessing her current financial situation. She has a modest savings account, some investments in a 401(k) plan through her employer, and owns her home. Her annual income is $80,000, and she estimates her annual retirement expenses will be approximately $50,000, adjusted for inflation. She sets a retirement savings goal of $1.5 million, factoring in inflation and potential investment growth. This goal is based on widely available retirement calculators and considers her desired lifestyle in retirement.

Investment Strategy and Asset Allocation

Sarah’s initial investment strategy is relatively conservative. She allocates 60% of her investment portfolio to bonds, 30% to stocks (primarily index funds for diversification), and 10% to cash. This reflects her risk tolerance at this stage of her life, prioritizing capital preservation over high-growth potential.

Visual Representation of Asset Allocation: Imagine a pie chart. Initially, the largest slice (60%) is labeled “Bonds,” representing her conservative approach. A medium-sized slice (30%) is labeled “Stocks,” and a smaller slice (10%) represents “Cash.” The colors could be blue for bonds, red for stocks, and green for cash.

Timeline of Key Events and Decisions

- Age 35-45: Focuses on consistent contributions to her 401(k) and maximizes employer matching. She gradually increases her stock allocation to 40% over this decade, reducing her bond allocation to 50%. Cash remains at 10%.

- Age 45-55: Sarah receives a significant bonus at work, allowing her to make a substantial lump-sum contribution to her retirement accounts. She evaluates her investment portfolio and rebalances it to 50% stocks, 40% bonds, and 10% cash. She also explores additional investment options, such as a Roth IRA.

- Age 55-65: Sarah begins to reduce her stock allocation slightly to 40%, increasing her bond allocation to 50% to mitigate risk closer to retirement. She continues to make regular contributions and carefully monitors her portfolio’s performance. She begins to explore options for annuities and other guaranteed income streams.

Visual Representation of Asset Allocation Over Time: Imagine a series of pie charts, one for each 10-year period. The initial chart (age 35-45) shows a larger bond allocation, gradually shifting towards a larger stock allocation in subsequent charts. The final chart (age 55-65) shows a shift back towards a more conservative allocation with a higher percentage in bonds.

Adjustments and Contingencies

Throughout her planning journey, Sarah regularly reviews her retirement plan, adjusting it based on changes in her income, expenses, and investment performance. She accounts for potential unexpected events, such as job loss or significant healthcare expenses, by maintaining an emergency fund and considering long-term care insurance. She also periodically consults with a financial advisor to ensure her plan remains on track.

Last Point

Planning for retirement is a multifaceted journey requiring careful consideration and proactive planning. This guide has provided a framework for assessing your current situation, setting realistic goals, and developing a comprehensive strategy to ensure financial security in your retirement years. By understanding the various income sources, managing expenses, and navigating legal and tax implications, you can create a personalized plan that aligns with your unique circumstances. Remember, regular review and adjustment of your plan are crucial to adapt to life’s unexpected events and changing economic conditions. Embrace the process, and secure a future that reflects your aspirations.

Popular Questions

What is the difference between a 401(k) and a Roth IRA?

A 401(k) is a retirement savings plan sponsored by your employer, often with employer matching contributions. Contributions are tax-deductible, but withdrawals in retirement are taxed. A Roth IRA is a personal retirement account where contributions are made after tax, but withdrawals in retirement are tax-free.

When should I start planning for retirement?

The sooner the better! Ideally, you should begin planning as soon as you start earning an income, even if it’s just small contributions to a retirement account.

How much should I save for retirement?

There’s no one-size-fits-all answer. A general guideline is to aim to save at least 10-15% of your pre-tax income, but it depends on your lifestyle, expenses, and retirement goals.

What if I experience an unexpected job loss before retirement?

Having an emergency fund is crucial. If you lose your job, immediately reassess your retirement plan, explore options like reducing expenses, and consider seeking professional financial advice.

{kind=link}