Navigating a tax audit can feel daunting, but with proper preparation, it becomes significantly less stressful. This guide provides a step-by-step approach to organizing your financial records, understanding common audit issues, and effectively communicating with tax authorities or your tax professional. We’ll cover everything from creating a robust system for storing your financial documents to knowing your rights as a taxpayer and utilizing helpful software tools. Ultimately, the goal is to empower you with the knowledge and confidence to face a tax audit with preparedness and assurance.

From assembling essential financial documents and understanding common audit pitfalls to leveraging tax software and effectively communicating with professionals, this guide aims to equip you with the necessary tools and knowledge for a successful audit preparation. We’ll explore practical strategies to minimize audit risks and ensure a smooth process, whether you’re a small business owner or an individual taxpayer.

Understanding Tax Audit Preparation

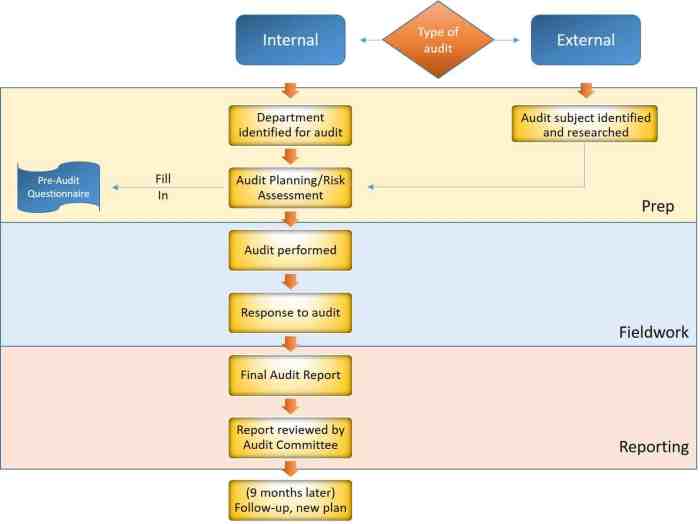

Preparing for a tax audit can seem daunting, but a systematic approach can significantly reduce stress and ensure a smooth process. Understanding the process and meticulously organizing your financial records are key to a successful audit. This section Artikels the steps involved in preparing for a tax audit and offers best practices for maintaining accurate financial documentation.

The overall process of tax audit preparation involves a series of steps, from gathering and organizing financial records to preparing for potential questions from the auditor. A well-prepared taxpayer can confidently present their financial information, demonstrating compliance with tax laws and minimizing the risk of penalties or adjustments.

Key Stages in Tax Audit Preparation

Preparing for a tax audit involves several distinct stages. Each stage builds upon the previous one, culminating in a comprehensive and well-organized presentation of financial information to the auditor. Failing to adequately address one stage can significantly impact the efficiency and outcome of the audit.

- Notification and Initial Assessment: Upon receiving notification of an audit, immediately assess the scope of the audit and the period under review. This helps you determine which records will be necessary.

- Record Gathering and Organization: This is the most crucial stage. Systematically collect all relevant financial documents, ensuring they are complete, accurate, and easily accessible. This may involve gathering bank statements, receipts, invoices, contracts, and tax returns.

- Documentation Review and Reconciliation: Carefully review all gathered documents, checking for accuracy and consistency. Reconcile bank statements with financial records and identify any discrepancies. This helps to proactively address potential issues.

- Preparation of Supporting Documentation: Organize all documents into a logical structure, making it easy for the auditor to review. Consider creating a detailed index or using labeled folders to facilitate efficient retrieval of specific information.

- Audit Meeting Preparation: Prepare for the audit meeting by reviewing all documentation and anticipating potential questions. Having a clear understanding of your financial situation will help you confidently respond to any queries.

Step-by-Step Guide for Organizing Financial Records

Organizing your financial records is paramount. A systematic approach ensures efficiency and reduces the likelihood of overlooking crucial information during the audit. The following steps provide a structured approach to record organization.

- Create a Centralized System: Establish a single, organized system for storing all financial documents. This could be a dedicated filing cabinet, cloud storage, or a combination of both.

- Categorize Documents: Organize documents by type (e.g., bank statements, receipts, invoices) and year. Using a consistent naming convention for files will improve searchability.

- Maintain Accurate Records: Ensure all records are accurate and complete. Double-check for errors and missing information. This includes verifying dates, amounts, and descriptions.

- Utilize Technology: Leverage accounting software or spreadsheet programs to track income and expenses, generating reports that summarize your financial activities. This can greatly simplify the audit process.

- Regularly Backup Data: Regularly back up all financial records to prevent data loss. This is especially important given the potential impact of data loss on an audit.

Best Practices for Maintaining Accurate and Complete Financial Documentation

Maintaining accurate and complete financial documentation is a continuous process, not just something to be done before an audit. Proactive record-keeping significantly reduces the stress and effort involved in preparing for a tax audit. Consistent and diligent record-keeping practices are essential.

- Keep original documents: Retain original receipts, invoices, and other supporting documents. Digital copies are helpful but originals provide stronger evidence.

- Maintain detailed records: Record all transactions accurately, including dates, descriptions, and amounts. Vague entries make it difficult to verify information during an audit.

- Reconcile accounts regularly: Regularly reconcile bank and credit card statements with your financial records to identify and correct any discrepancies promptly.

- Use a consistent accounting method: Adopt and consistently apply a suitable accounting method (cash or accrual) throughout the year. Inconsistency can lead to confusion and errors.

- Consult a tax professional: Seek advice from a qualified tax professional for guidance on maintaining accurate and compliant financial records.

Gathering and Organizing Financial Records

A well-organized system for your financial records is crucial for a smooth tax audit. Efficient record-keeping minimizes stress and ensures you can quickly provide the necessary documentation to the auditor. This section details essential steps in gathering, organizing, and reconciling your financial information.

Essential Financial Documents Checklist

Preparing for a tax audit involves gathering comprehensive financial documentation. A missing document can significantly delay the process. This checklist ensures you have all necessary materials readily available.

- Tax returns from previous years.

- Bank statements (checking, savings, and money market accounts) for the relevant tax year.

- Credit card statements for the relevant tax year.

- Payroll records (W-2s, pay stubs, 1099s).

- Investment records (brokerage statements, 1099-DIV, 1099-INT, K-1 forms).

- Receipts for business expenses (including detailed descriptions and dates).

- Invoices issued to clients or customers.

- Loan documents (mortgages, auto loans, business loans).

- Property tax statements.

- Insurance policies and records of payments.

- Records of charitable donations (with substantiation).

- Depreciation schedules for business assets.

Organizing and Storing Financial Records

A robust system for storing financial records—both physically and electronically—is essential for efficient retrieval during an audit. Consider both the security and accessibility of your chosen methods.

Electronic Storage: Utilize cloud-based storage services or external hard drives to create secure backups of your digital records. Organize files using a clear folder structure (e.g., by year, by document type). Consider using accounting software to manage and store your financial data electronically.

Physical Storage: If you maintain physical records, use labeled file folders and a filing system that allows for easy retrieval. Store documents in a secure, climate-controlled environment to protect against damage. Consider scanning important documents to create digital backups.

Bank and Credit Card Statement Reconciliation

Reconciling bank and credit card statements with your accounting records is a critical step in ensuring accuracy. Discrepancies can indicate errors in record-keeping or potential fraudulent activity.

The process involves comparing transactions listed on your bank and credit card statements with the corresponding entries in your accounting software or ledger. Any discrepancies should be investigated and corrected. This process helps identify missing transactions, incorrect amounts, and potential accounting errors. For example, if a deposit of $1000 is recorded in your accounting software but only $950 appears in your bank statement, you would need to investigate the $50 difference.

Tracking and Documenting Income and Expense Transactions

Maintaining detailed records of all income and expense transactions is crucial for accurate tax reporting and successful audit preparation. This includes meticulous record-keeping of both business and personal finances, depending on the scope of the audit.

Methods for tracking income and expenses include using accounting software, spreadsheets, or dedicated expense tracking apps. Ensure each transaction includes a date, description, amount, and relevant supporting documentation (e.g., receipts, invoices). Regularly review and reconcile your records to ensure accuracy and identify any potential discrepancies. For example, a business owner should meticulously track all sales invoices, client payments, and business expenses, including travel costs, office supplies, and marketing expenditures.

Common Tax Audit Issues and Their Solutions

Navigating a tax audit can be stressful, but understanding common issues and proactive strategies can significantly reduce anxiety and potential penalties. This section highlights frequent areas of concern during tax audits, offering solutions and preventative measures to ensure compliance. Preparation is key to a smoother audit process.

Common Areas of Concern During Tax Audits

Several areas consistently attract attention from tax auditors. These include discrepancies in reported income, deductions claimed, and the accurate classification of business expenses. Auditors often scrutinize the supporting documentation for each claimed deduction to ensure it meets the IRS guidelines. Failure to maintain meticulous records significantly increases the risk of audit issues. Another frequent concern involves the proper reporting of capital gains and losses, requiring detailed documentation of asset acquisition and disposal dates and costs. Finally, the accuracy of the reported business mileage is frequently examined, with many businesses inadvertently misreporting or lacking proper documentation.

Addressing Discrepancies in Financial Records

When discrepancies arise, a calm and organized approach is crucial. Begin by meticulously reviewing all relevant financial documents, including bank statements, invoices, receipts, and tax returns. Compare these records against the information reported on your tax return, identifying any inconsistencies. If discrepancies exist, prepare a detailed explanation outlining the circumstances leading to the difference. This explanation should provide supporting evidence, such as corrected invoices or amended bank statements. If the discrepancy is due to an error, promptly correct it and file an amended tax return (Form 1040-X). Open communication with the auditor is also essential; providing clear and concise explanations demonstrates your cooperation and commitment to resolving the issue. Maintaining a professional and respectful demeanor throughout the process is highly recommended.

Examples of Common Mistakes to Avoid During Tax Preparation

Many tax-related errors stem from simple oversights or misunderstandings. One common mistake is failing to accurately track and categorize business expenses. Mixing personal and business expenses is another frequent error, making it difficult to determine the appropriate deductions. Improperly claiming deductions, such as exceeding allowable limits for charitable contributions or home office expenses, is another prevalent issue. Finally, neglecting to maintain adequate records for all transactions, especially those involving large sums of money, significantly increases the risk of an audit. Accurate record-keeping is fundamental to a successful tax filing.

Proactive Measures to Minimize Audit Risks

Proactive steps can significantly reduce the likelihood of an audit. This begins with meticulous record-keeping; maintaining organized and easily accessible financial records is crucial. This includes retaining receipts, invoices, bank statements, and other supporting documentation for at least three years, and ideally longer. Seeking professional tax advice from a qualified accountant or tax advisor can help prevent errors and ensure compliance with all relevant tax laws and regulations. Regularly reviewing your tax returns and comparing them to your financial records can help identify and correct potential errors before they become audit issues. Finally, staying informed about current tax laws and regulations helps you avoid unintentional mistakes. Staying current with tax law changes is a key element of tax compliance.

Preparing for an IRS Audit (or other relevant tax authority)

An IRS audit, while potentially stressful, is a manageable process with proper preparation. Understanding your rights, gathering necessary documentation, and approaching the audit strategically can significantly improve the outcome. This section details the steps to take when facing an audit, Artikels your taxpayer rights, and provides guidance on effective communication with the auditor.

Responding to an Audit Notification

Upon receiving an audit notification, carefully review the letter’s contents. Note the type of audit (correspondence, office, or field), the tax years under review, and the requested documents. Promptly acknowledge receipt, confirming your understanding of the requirements. This demonstrates cooperation and professionalism. Begin immediately gathering the requested documentation, organizing it systematically for easy access during the audit process. Contacting a tax professional at this stage is highly advisable, especially for complex tax situations.

Taxpayer Rights During an Audit

Taxpayers possess several crucial rights during an audit. These rights include the right to be represented by a tax professional (CPA, enrolled agent, or attorney), the right to request an explanation of the auditor’s findings, the right to examine the evidence used by the IRS, and the right to appeal any adverse decisions. Furthermore, taxpayers have the right to remain silent and are not obligated to provide information that could incriminate them. Understanding these rights empowers taxpayers to navigate the audit process confidently and protect their interests.

Questions to Ask the Auditor

A proactive approach to the audit involves preparing questions for the auditor. These questions should focus on clarifying the specifics of the audit, understanding the basis for the IRS’s concerns, and seeking clarity on procedures. Examples include questions about the specific items under review, the evidence the IRS is relying upon, and the timeline for the audit process. Asking clarifying questions demonstrates engagement and helps to ensure a thorough and fair assessment. However, avoid confrontational questions or those that are clearly answered in the audit notification.

Sample Response to an Audit Request for Information

A prompt and organized response to the IRS’s information request is crucial. A sample response could begin with acknowledging receipt of the audit notice, listing the enclosed documents, and confirming the taxpayer’s willingness to cooperate fully. The response should then detail the location of each requested document, and it should offer to provide additional information or clarification if needed. For example, if a specific invoice is requested, the response might state: “The invoice referenced as Item 3 on your request is enclosed. A copy of the corresponding bank statement showing payment is also included for your review.” Maintaining a professional and cooperative tone throughout the response is key.

Utilizing Tax Software and Tools

Navigating the complexities of tax preparation, especially when facing an audit, is significantly eased by leveraging the power of tax software and data analytics tools. These tools not only streamline the process of record-keeping and report generation but also proactively help identify potential audit risks. Choosing the right software and understanding its capabilities are crucial steps in effective tax audit preparation.

Tax preparation software offers a range of features designed to simplify the tax filing process and improve accuracy. These features can be broadly categorized into data entry, calculation, report generation, and risk assessment functionalities. Understanding these features and how they can be applied during an audit preparation is key to efficient and successful compliance.

Tax Software Comparison and Feature Selection

Several reputable tax preparation software options cater to various needs and budgets, ranging from simple programs for individual filers to sophisticated solutions for businesses with complex financial structures. Factors to consider when selecting software include the level of complexity of your tax situation, the types of reports needed, the level of user support offered, and the software’s integration capabilities with other accounting tools. For example, TurboTax offers various tiers, from basic individual filing to more comprehensive options for businesses and self-employed individuals. TaxAct provides similar tiered services, while H&R Block’s software offers a similar range of options, each with varying features and price points. A thorough comparison of these options, considering your specific needs, will help you make an informed decision.

Generating Audit-Ready Reports Using Tax Software

Tax software facilitates the generation of numerous reports essential for a tax audit. These reports typically include balance sheets, income statements, profit and loss statements, and detailed schedules supporting various tax deductions and credits. The software automates the process of compiling this information, reducing manual effort and minimizing the risk of errors. For example, many programs allow for the direct import of data from bank accounts and other financial institutions, significantly speeding up the data entry process. Moreover, the software usually provides the ability to easily export reports in various formats (PDF, CSV, etc.) suitable for submission to the tax authorities. The ability to easily generate these reports in a standardized format is a significant advantage during an audit.

Utilizing Data Analytics Tools for Audit Risk Identification

Data analytics tools, often integrated within or compatible with tax preparation software, play a crucial role in proactive audit risk assessment. These tools can analyze large datasets of financial information to identify unusual patterns or anomalies that might trigger an audit. For instance, a significant and unexplained increase in certain deductions compared to previous years might be flagged as a potential risk. These tools can also help in identifying inconsistencies within the financial records, ensuring accuracy and completeness before filing. Proactive identification and mitigation of such risks significantly reduce the likelihood of facing an audit or negative consequences during one.

Effective Tax Software Management of Financial Records

Effective use of tax software for managing financial records involves organizing data in a structured manner, regularly backing up data, and maintaining accurate records of all transactions. This includes properly categorizing expenses, ensuring accurate recording of income, and maintaining supporting documentation for all transactions. The software’s features for data import, organization, and categorization should be fully utilized. Regular reconciliation of bank statements and other financial records with the data entered into the software is crucial for maintaining accuracy and identifying potential discrepancies early on. This proactive approach to record-keeping not only simplifies tax preparation but also significantly strengthens your position in the event of an audit.

Working with a Tax Professional

Navigating the complexities of a tax audit can be daunting, even for those well-versed in tax law. Engaging a qualified tax professional significantly increases your chances of a successful outcome, minimizing stress and potential financial penalties. Their expertise provides a crucial advantage throughout the entire audit process.

A tax professional offers invaluable support and guidance during tax audit preparation and the audit itself. Their deep understanding of tax codes, regulations, and audit procedures ensures a more efficient and effective approach than attempting to handle the process alone.

Benefits of Engaging a Tax Professional for Audit Preparation

Tax professionals possess specialized knowledge and experience in handling tax audits. They can identify potential issues early on, helping you prepare comprehensive and accurate documentation. This proactive approach significantly reduces the likelihood of facing significant penalties or protracted disputes with the tax authorities. Furthermore, their representation during the audit process provides a crucial buffer, allowing you to focus on other aspects of your business or personal life. They can effectively communicate with the auditors, ensuring your position is clearly understood and fairly considered. The peace of mind that comes with professional representation is invaluable.

Services Provided by a Tax Professional During an Audit

Tax professionals provide a wide range of services during an audit. This includes reviewing your financial records for accuracy and completeness, identifying and addressing any potential discrepancies or inconsistencies. They will prepare and submit all necessary documentation to the tax authorities, meticulously organizing and presenting information in a clear and concise manner. They act as your primary point of contact with the auditors, effectively communicating your position and negotiating on your behalf. Furthermore, they can represent you at any meetings or hearings related to the audit. Their expertise extends to explaining complex tax laws and regulations, ensuring a thorough understanding of the audit process.

Questions to Ask When Selecting a Tax Professional

Choosing the right tax professional is crucial. Before engaging their services, it’s important to clarify their experience with tax audits, specifically those involving situations similar to your own. Inquire about their fees and payment structure to avoid unexpected costs. Understand their communication style and responsiveness, ensuring a clear and consistent flow of information. Ask about their success rate in resolving tax audit disputes and their familiarity with relevant tax laws and regulations. It’s also prudent to request references from past clients to gauge their professionalism and effectiveness. Finally, confirm their qualifications and licensing status to ensure they are legally authorized to represent you.

Tips for Effective Communication with a Tax Professional

Open and honest communication is essential for a successful working relationship with your tax professional. Provide them with all necessary documentation promptly and completely. Clearly articulate your concerns and questions, ensuring you thoroughly understand their advice and recommendations. Maintain regular contact to discuss the progress of the audit and address any emerging issues. Promptly respond to their requests for information. Building a strong rapport based on trust and mutual understanding is key to navigating the audit process effectively.

Post-Audit Procedures

Completing a tax audit is a significant step, but the process doesn’t end there. Understanding post-audit procedures is crucial for ensuring a fair outcome and preventing future issues. This section details the necessary steps to take after an audit concludes, covering appeals, potential outcomes, and strategies for future tax compliance.

Following a tax audit, several critical steps are essential to manage the outcome effectively and plan for future tax compliance. These steps encompass reviewing the audit findings, understanding your options for appeal, and implementing strategies to minimize future audit risks.

Reviewing the Audit Findings

Carefully review the audit report to understand the adjustments made and the reasons behind them. Compare the report to your original tax return and supporting documentation. Identify any discrepancies or areas of disagreement. If you need clarification on any aspect of the report, don’t hesitate to contact the auditor or your tax professional. This thorough review forms the basis for any potential appeal.

Appealing an Audit Decision

If you disagree with the auditor’s findings, you have the right to appeal. The appeal process varies depending on the tax authority (IRS, state tax agency, etc.). Generally, it involves filing a formal appeal within a specified timeframe, often including a detailed explanation of your disagreement and supporting evidence. This may involve gathering additional documentation, consulting with a tax attorney or CPA, and potentially participating in a formal hearing or conference. For example, with the IRS, an appeal might start with an informal meeting with the auditor’s supervisor, followed by a formal appeal to the Appeals Office if the issue isn’t resolved.

Common Outcomes of a Tax Audit

Tax audits can result in several different outcomes. The most common include:

- No Change: The audit confirms the accuracy of your original return, and no adjustments are made.

- Agreed Adjustments: You and the auditor agree on adjustments to your return, resulting in a change to your tax liability (either an increase or a decrease).

- Disputed Adjustments: You and the auditor disagree on some or all of the adjustments, potentially leading to an appeal process.

- Penalty Assessment: If the audit reveals intentional or negligent errors, penalties may be assessed in addition to any tax owed.

For instance, a small business owner might experience an agreed adjustment if they incorrectly categorized certain expenses, while a high-net-worth individual might face a disputed adjustment and potential penalties if the audit reveals undisclosed income.

Preventing Future Audit Issues

Proactive measures significantly reduce the likelihood of future audits. Maintaining accurate and organized financial records, using reputable tax software, and seeking professional tax advice are crucial preventative steps.

Specifically, maintaining detailed records for all income and expenses, including receipts, invoices, and bank statements, is vital. Using tax preparation software with built-in error checks can also help identify and correct potential problems before filing. Regular consultations with a qualified tax professional can ensure compliance with all applicable tax laws and regulations, significantly reducing audit risk.

Illustrative Example: A Small Business Tax Audit

This section details a hypothetical tax audit scenario for a small business, illustrating the process from initial notification to resolution. The example focuses on common issues and the importance of meticulous record-keeping. Understanding this scenario can help small business owners better prepare for their own audits.

Hypothetical Scenario: “The Cozy Coffee Shop” Audit

The Cozy Coffee Shop, a small café owned and operated by Sarah Miller, received a notice from the IRS scheduling a tax audit for the 2022 tax year. The audit was triggered by a discrepancy between the shop’s reported income and the estimated income based on industry averages and reported sales of similar businesses in the area. Sarah, while maintaining detailed sales records, had not meticulously tracked all expenses, particularly those related to minor repairs and supplies.

Financial Records Involved

The audit focused on several key areas of The Cozy Coffee Shop’s financial records. These included:

- Sales Records: Daily sales logs, point-of-sale (POS) system data, and bank statements showing deposits.

- Expense Records: Invoices, receipts, bank statements showing payments, and a general ledger.

- Inventory Records: Records showing beginning and ending inventory, purchases, and cost of goods sold (COGS).

- Payroll Records: Payroll tax returns, W-2 forms for employees, and records of employee wages and deductions.

- Depreciation Records: Records of assets purchased, their useful lives, and depreciation methods used.

Sarah’s relatively complete sales records contrasted sharply with her less organized expense records. Many small expenses were documented only on crumpled receipts or not at all. This lack of detailed expense documentation was the main point of contention during the audit.

Preparing for and Responding to the Audit

Upon receiving the audit notice, Sarah immediately gathered all relevant financial records. She organized them chronologically and by category, creating separate folders for each type of document. She also consulted with a tax professional who reviewed her records and advised her on the best approach to respond to the IRS’s inquiries. The tax professional helped Sarah reconstruct some missing expense records based on bank statements and other available information.

Audit Timeline

| Date | Event | Documents Involved | Outcome |

|---|---|---|---|

| March 15, 2024 | IRS Audit Notice Received | Audit notice letter | Sarah contacts her tax professional. |

| April 1, 2024 | Initial Meeting with IRS Agent | Sales records, bank statements | Agent expresses concerns about expense recordkeeping. |

| April 15, 2024 | Submission of Additional Documents | Reconstructed expense records, receipts, invoices | Agent reviews submitted documents. |

| May 10, 2024 | Follow-up Meeting | All financial records, explanations of discrepancies | Agent acknowledges improvements in documentation. |

| June 1, 2024 | Audit Completion Notice | Final audit report | Minor adjustments made to Sarah’s tax return; no penalties assessed. |

Final Review

Successfully preparing for a tax audit involves proactive planning, meticulous record-keeping, and a clear understanding of your rights. By following the steps Artikeld in this guide, you can significantly reduce stress and increase your chances of a positive outcome. Remember, preparedness is key – taking proactive measures to organize your finances and understand potential audit issues will greatly benefit you throughout the entire process. Don’t hesitate to consult with a tax professional for personalized guidance and support.

Q&A

What happens if I don’t have all the requested documents?

Explain the situation honestly to the auditor. Request an extension if needed, providing a realistic timeframe for obtaining missing documents. Failure to comply can lead to penalties.

Can I represent myself during a tax audit?

Yes, you have the right to represent yourself. However, engaging a tax professional is often advisable for complex audits.

How long does a tax audit typically take?

The duration varies greatly depending on the complexity of your tax return and the issues raised by the auditor. It can range from a few weeks to several months.

What are the penalties for tax evasion?

Penalties can include significant fines, interest charges, and even criminal prosecution depending on the severity and intent.

{kind=link}